The development of cold chain infrastructure is crucial for a country like India, which has a large agricultural sector and a significant need for efficient storage and transportation of perishable goods such as fruits, vegetables, dairy products, and pharmaceuticals. Government policies and initiatives play a key role in the large-scale development of cold chain infrastructure in India. The Indian government recognizes the importance of cold chain infrastructure and has implemented various policies and initiatives to promote its large-scale development.

One of the key approaches taken by the Indian government is the introduction of subsidies and grants-in-aid to incentivize the establishment of cold chain facilities. These financial incentives aim to offset the high capital costs involved in setting up cold storage units, refrigerated transportation, and other infrastructure components. The subsidies help reduce the financial burden on entrepreneurs and encourage private sector participation in cold chain development.

These flagship programmes promote the development of complete end-to-end cold chains, from the source to the end-customer. These initiatives aim to bridge the gaps in the existing supply chain and ensure the seamless movement of perishable goods. Some of these programs include:

- Mission for Integrated Development of Horticulture (MIDH)

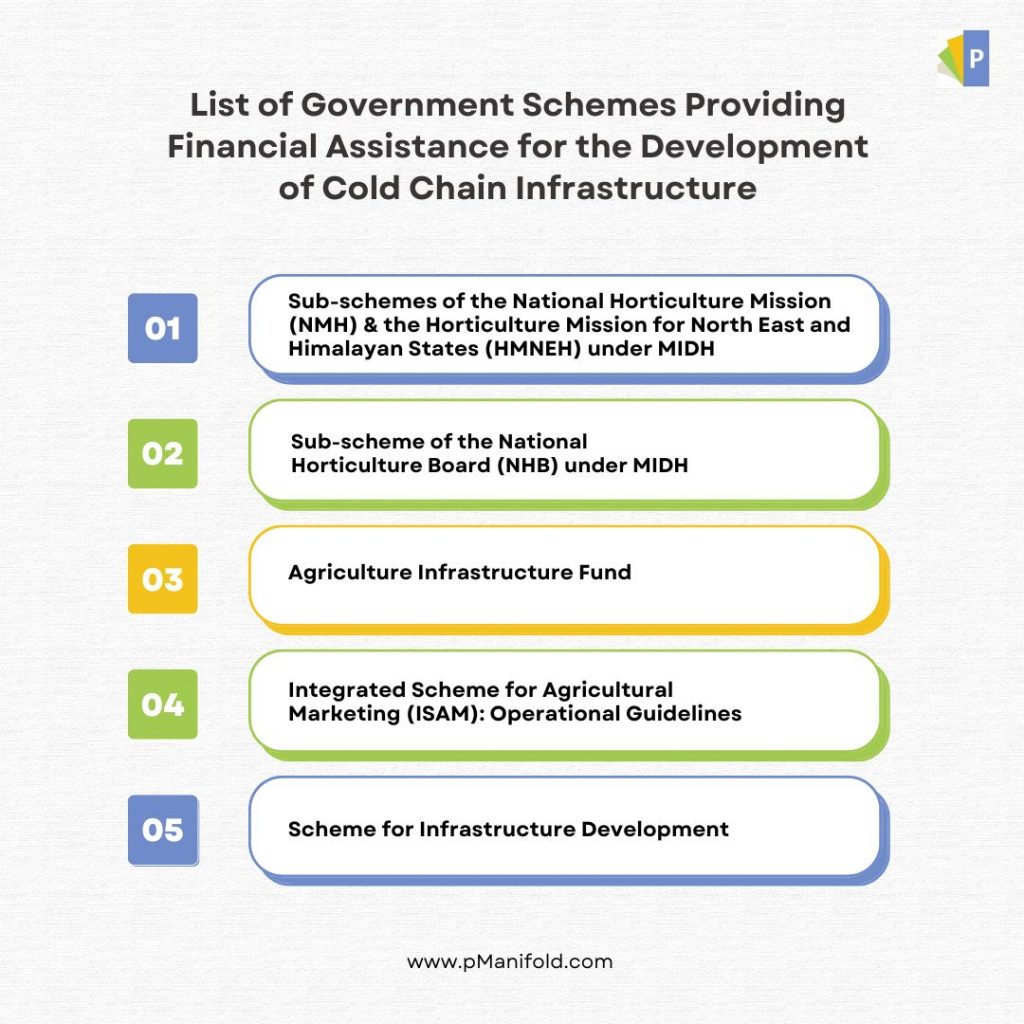

MIDH is a government scheme for holistic growth of the horticulture sector ((fruits, vegetables, root and tuber crops, mushrooms, spices, flowers, aromatic plants, coconuts, cashews, cocoa and bamboo shoots). It provides financial assistance, including for cold storage. Subsidies of 35% (or 50% in hilly areas) are available. MIDH helps establish energy-efficient multi-chamber cold storage units with thermal insulation, humidity control, advanced cooling systems, and automation. Long-term storage hubs up to 5,000 MT capacity are covered by NHM/HMNEH, while 5,000-10,000 MT hubs are covered by NHB scheme.

- National Horticulture Mission (NHM) / Horticulture Mission for North East and Himalayan States (HMNEH)

Long-term cold storage and distribution hubs of up to 5,000 MT capacity are eligible for assistance under this open-ended sub-scheme of MIDH. Assistance comes in the form of credit linked subsidies, amounting to 35% of the capital cost of the project, or 50% in NE, hilly and Scheduled Areas.

- National Horticulture Board (NHB)

The National Horticulture Board (NHB) is implementing the “Capital Investment Subsidy for Construction/Expansion/ Modernisation of Cold Storages and Storages for Horticulture Products.” Under this scheme (a sub-scheme of MIDH), assistance is available for the installation and modernization of cold storage units with capacity between 5,000 MT and 10,000 MT. This is an open-ended credit-linked programme offering subsidies amounting to 40% of the capital cost of a project (limited to INR 30 lakhs per project), or 50% in NE, hilly areas and Scheduled Areas (limited to INR 37.50 lakhs per project) sub-scheme of MIDH. Assistance comes in the form of credit-linked subsidies amounting to 35% of the capital cost of the project, or 50% in NE, hilly and Scheduled Areas.

- Pradhan Mantri Kisan SAMPADA Yojana (PMKSY)

SAMPADA stands for Scheme for Agro-Marine Processing and Development of Agro-Processing Clusters. It consists of a comprehensive package to create modern infrastructure and efficient supply chain management from farmgate to retail outlet, with the goal of boosting the growth of the food processing sector and improving returns for farmers. This is in line with the GoI’s goal to double farmers’ income, creating significant employment opportunities in rural areas. It also reduces food waste, using efficient and modern technology to help the food processing industry and export houses convert surplus produce into an export commodity.

The following will be developed under PMKSY:

- Mega Food Parks

- Integrated cold chain and value addition infrastructure

- Creation, expansion and modernization of food processing and preservation capacities

- Infrastructure for agro-processing clusters

- Backward and forward linkages

- Food safety and quality assurance infrastructure

- Human resources and institutions

So far, the Ministry has approved 41 Mega Food Parks, 353 cold chain projects, 63 agro-processing clusters, 292 food processing units, 63 backward and forward linkages projects and 6 Operation Green projects across the country.

- Scheme for Integrated Cold Chain, Value Addition and Preservation Infrastructure

Part of PMKSY, this scheme is implemented by the Ministry of Food Processing Industries (MOFPI) with the aim of reducing post-harvest produce losses and providing better prices to farmers for their produce. Financial assistance (grants-in aid) is limited to a maximum of INR 10 crore per project for technical civil works, eligible plants and machinery, subject to the following conditions:

- For storage infrastructure (including packhouses, pre-cooling units, ripening chambers and transport infrastructure), grants-in-aid are provided amounting to 35% of total project cost, or 50% for NE and Himalayan States, Integrated Tribal Development Project (ITDP) Areas and islands.

- For value addition and processing infrastructure (including frozen storage and deep freezers integral to processing), grants-in-aid are provided amounting to 50%, or 75% for NE and Himalayan States, ITDP Areas and islands.

- For irradiation facilities, grants-in-aid are provided amounting to 50%, or 75% for NE and Himalayan States, ITDP Areas and islands.

- For reefer vehicles, credit-linked back-ended grants-in-aid are provided amounting to 50% of the cost of a new reefer vehicle/mobile pre-cooling van, up to a maximum of INR. 50.00 lakh. Integrated cold chain and preservation infrastructure can be set up by individuals, groups of entrepreneurs, cooperative societies, Self Help Groups (SHGs), Farmer Producer Organisations (FPOs), NGOs or central/state PSUs. Standalone cold storage units are not covered under the scheme.

- Small Farmer Agri-Business Consortium (SFAC) Assistance

These subsidies are available for cold storage facilities set up as part of an integrated value chain project, provided the cold storage component accounts for no more than 75% of the Total Financial Outlay (TFO). Subsidies can amount to 25% of the capital cost of a project with a maximum ceiling of INR 2.25 crores, or 33.33% with a ceiling up to INR 4 crores in NE, hilly and Scheduled Areas.

In order to meet the government’s goal of doubling farmers’ income by 2022, several market reforms are being rolled out to encourage the development of CCI:

- The establishment of 22,000 Gramin Agriculture Markets (GrAMs) to act as aggregation platforms

- An Agri-Export Policy, which aims to double agri-exports by 2022

- The promotion of 10,000 FPOs by 2024

- The creation of the following Corpus Funds:

- An agri-marketing fund to strengthen eNAM6 and GrAMs (INR. 2,000 crores)

- An Agricultural Infrastructure Fund (AIF) to provide collateral-free loans with an interest subvention of 3% (INR. 100,000 crores)

Apart from this, the government is also providing profit-linked tax holidays, priority sector lending, and lower tax rates for raw and processed products. Cold chain services – including pre-conditioning, pre-cooling, ripening, waxing and retail packing – are also exempt from Goods and Service Tax (GST).

Some of the other key government initiatives in the cold chain sector are as follows:

- Exemption from Customs and Excise Duty

- Customs Duty: A concessional basic customs duty (BCD) of only 5% is applied for cold storage, cold room and industrial projects (including farm-level precooling) for the preservation, storage or processing of agricultural, horticultural, dairy, poultry, aquatic and marine produce and meat. Truck refrigeration units and other refrigerated vehicles are fully exempted from BCD.

- Excise Duty: Central excise duty has been fully exempted for the installation of cold storage, cold rooms and refrigerated vehicles for the preservation, storage, transport and processing of agricultural, apiary, horticultural, dairy, poultry, aquatic and marine produce and meat. This also applies to air conditioning equipment and refrigeration panels for cold chain infrastructure, including conveyor belts used in cold storage units, mandis and warehouses.

- Foreign Direct Investment (FDI):

100% FDI is allowed, leading to an increase in private sector investment. This policy requires a minimum investment of US$100, with at least 50% invested in back-end infrastructure.

- Fiscal Incentives for Cold Chain”

- Section 80-IB of the Income Tax Act provides deductions for cold chain-related industrial activity. Deductions apply to 100% of profits for the first five years, then 25-30% for the next five years.

- Under Section 35-AD of the Income Tax Act 1961, deductions of 150% are permitted for expenditure incurred in setting up a cold chain facility.

These government initiatives aim to reduce post-harvest losses, improve farmers’ income, create employment opportunities, and enhance the overall efficiency of the agricultural supply chain.

GOI’s schemes and initiatives to support cold chain infrastructure signify its commitment to fostering efficient storage and transportation of perishable goods. By providing subsidies, grants, and incentives, the government encourages private sector participation, reduces post-harvest losses, and promotes the overall growth of the agricultural sector. These efforts align with broader goals of doubling farmers’ income, boosting food processing, and enhancing the efficiency of the supply chain. Overall, the government’s focus on cold chain development contributes to the economic growth and sustainability of India’s agricultural industry.

List of Government Schemes Providing Financial Assistance for CCI Development