The concept of voluntary carbon markets has been around for decades, gaining more recognition among climate activists than among leaders in politics and the financial community. The Kyoto Protocol in 1997 marked the initial phase where international involvement in carbon markets began to see broader acceptance with more than 150 nation signatories.

The world has evolved considerably, recognizing climate action as an urgent step to restore and rehabilitate the planet. Offsetting emissions plays an important role as a supplementary strategy in the decarbonization efforts of numerous companies, particularly addressing residual emissions in challenging-to-abate sectors (steel, cement, thermal power plants, etc)

Carbon markets represent a key tool in addressing the challenge of climate change, which involves reducing the accumulation of greenhouse gases (GHG) in the atmosphere. The participation of Designated Consumers (DC) in compliance with the Perform, Achieve, and Trade (PAT) scheme has brought the spotlight to this approach in India, making it a topic of discussion and consideration among others.

A carbon credit serves as an offset mechanism issued for an equivalent reduction or absorption of carbon emissions from the atmosphere, resulting from a targeted carbon reduction project. These are issued to anyone aiming to reduce their carbon footprint.

“1 carbon credit = 1 tonne of CO2”

Carbon markets on the other hand are trading systems in which carbon credits are sold and bought. Companies or individuals can use carbon markets to compensate for their GHG emissions by purchasing carbon credits from entities that remove or reduce GHG emissions. To get a better view, one tradable carbon credit equals one tonne of carbon dioxide or the equivalent amount of a different greenhouse gas reduced, sequestered or avoided. When a credit is used to reduce, sequester, or avoid emissions, it becomes an offset and is no longer tradable.

“Issued carbon credits are certified and verified emissions reductions available for sale, listed on carbon registries. Retired carbon credits, once purchased, can no longer be traded, or bought by any entity, with some being bought to retire later.”

Methane is a highly potent greenhouse gas with a global warming potential of 25 times that of carbon dioxide. Thus, the reduction of one ton of methane is equivalent to 25 tons of carbon dioxide.

One metric ton of Methane avoided is equivalent to 25 carbon credits[1]

Growing consumer pressure and the introduction of mandatory emissions trading programs have compelled companies to explore the voluntary carbon offset market. In the context of international regulations, there is an increasing necessity for companies and investors to enhance their understanding of carbon credits. Additionally, a carbon market facilitates the simultaneous trading of both carbon credits and carbon offsets for investors and corporations.

A Brief History of Carbon Markets

The concept of voluntary carbon markets has been around for decades, gaining more recognition among climate activists than among leaders in politics and the financial community.

The Kyoto Protocol in 1997 marked the initial phase where international involvement in carbon markets began to see broader acceptance with more than 150 nations as signatories. Parties with commitments under the agreement agreed to limit or reduce their greenhouse gas emissions between 2008 – 2012 to 5.4% which was well below the levels of 1990. Emissions trading, as set out in the Kyoto Protocol, allowed countries to sell the excess capacity of emission units to countries that had levels well over their targets.[2]

The Protocol also laid the foundation and groundwork for Market-Based Instruments (MBIs), including the Clean Development Mechanism (CDM). This mechanism enabled countries with emission reduction commitments to undertake or finance projects in the developing world, earning tradable certified emission reduction (CER) credits to achieve Kyoto targets.

It is since then almost the entire world – both developed and developing countries started formulating carbon emissions standards and guidelines for controlling harmful gas emissions.

At present, carbon markets are undergoing big changes due to the implementation of international governmental cooperation for exchanging emission reductions. This cooperation is being implemented under Article 6 of the Paris Agreement enabling countries to voluntarily work together to fulfill emission reduction targets outlined in their Nationally Determined Contributions (NDCs).

Types: Mandatory and Voluntary

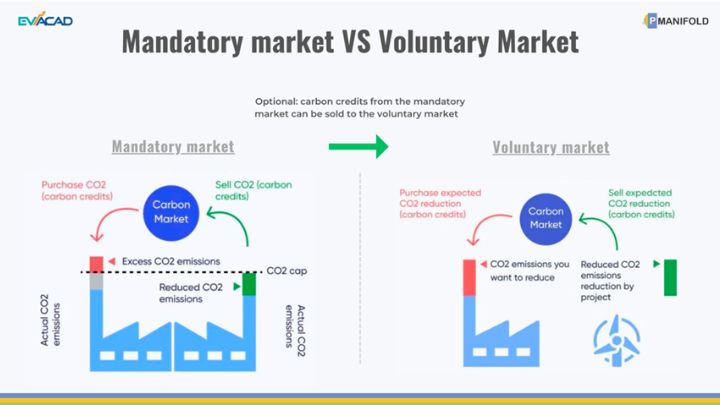

They are broadly divided into two types of carbon markets –compliance and voluntary.

Compliance markets are created as a result of any national, regional, and/or international policy or regulatory mandates, with global agreements like the Kyoto Protocol or the Paris Climate Change Accord establishing the limits. These markets are instituted and overseen by obligatory national, regional, or international carbon reduction frameworks.

To enable the countries to take steps to lower their emissions can be achieved either by implementing a carbon tax or establishing a compulsory carbon market. The central components of these markets are referred to as Compliance Emission Reduction (CER) credits.

Examples of mandatory carbon markets: the European Union Emission Trading System (EU ETS), the Western Climate Initiative (WCI) & the Regional Greenhouse Gas Initiative (RGGI)

Voluntary carbon markets, both at the national and international levels, involve the issuance, purchase, and sale of carbon credits voluntarily. In these markets, companies and other entities proactively take actions to reduce their carbon footprint as part of their initiatives, driven by considerations like corporate social responsibility (CSR).

Voluntary markets operate independently of compliance markets, allowing companies and individuals to voluntarily purchase carbon offsets without any specific intention for compliance purposes. Voluntary carbon markets can also accelerate emission reduction efforts toward net zero and gain increasing interest from the private sector.

In simple words, the regulatory market is mandated, while the voluntary market is optional.

Source: Berkeley Carbon Trading Project

India is poised to introduce its country-level carbon market. The Carbon Credit Trading Scheme(CCTS) in the Indian Carbon Market (ICM) will enhance the energy transition efforts with an increased scope that will cover the potential energy-intensive sectors in India. For these sectors, GHG emissions intensity benchmarks and targets will be developed, which will be aligned with India’s emissions trajectory as per climate goals. It is envisaged that there will be a development of a voluntary mechanism concurrently, to encourage GHG reduction from non-obligated sectors.

Carbon credits from e-Mobility are an overlooked (potentially massive) contributor to implementing net-zero strategies.

Transport accounts for a quarter of global emissions, about 12 billion tCO2e/year, with road transport responsible for 70% of this figure. Despite the global commitment to achieving zero-emission targets by 2030-2050, there’s an increasing need for climate mitigation in both the energy and transport sectors. [3]

While carbon credits from renewable energy are prevalent, those from the transport sector are notably lacking. Electric mobility (e-Mobility) emerges as a pivotal solution, replacing fossil fuels with electricity and optimizing renewable energy use. E-Mobility presents a crucial opportunity to decarbonize both sectors. Despite the significant transport has on climate, the sector remains the most underrepresented in carbon finance, contributing less than 2% of the global carbon credits.

Battery EV technologies hold promise to change this landscape by expediting the generation of carbon credits from transport, raising awareness, and stimulating demand for such credits. Carbon finance mechanisms can potentially help project proponents overcome some key financial barriers, like high vehicle costs and a lack of charging infrastructure, by providing a financial reward for avoided emissions.

While compared to developed markets like the US, the Indian Carbon market is still in its initial stages, its CDM projects have helped India in developing projects that qualify for voluntary carbon credits.

[3]https://shellfoundation.org/app/uploads/2021/11/SouthPole-report.pdf

Bangkok E-Bus Programme

Switzerland and Thailand are currently implementing the first e-Mobility project under Article 6,[4] focusing on acquiring internationally transferred mitigation outcomes (ITMOs). The initiative, known as the Bangkok E-Bus Programme, targets the introduction of around 2,000 electric buses in the Bangkok Metropolitan Area. This strategic move aims to avoid approximately 500,000 tonnes of CO2 by 2030, offering a substantial contribution to air quality improvement in the congested megacity of Bangkok.

The program was commissioned by the KliK Foundation and is being implemented by South Pole, in partnership with the Thai company Energy Absolute.

Since November 2022, Switzerland has approved three offset programs. Two of these programs, developed by the United Nations Development Programme (UNDP), aim to reduce methane emissions from rice farming in Ghana and promote the use of decentralized mini-solar panels on outlying islands in Vanuatu. These initiatives align with the federal administration’s voluntary carbon offsetting efforts.

[4]https://www.alliancesud.ch/en/new-electric-buses-bangkok-no-substitute-climate-protection-switzerland

Article 6 of the Paris Agreement enables countries to collaborate voluntarily by transferring carbon credits to help each other achieve emission reduction targets. Specifically, 6.2 allows trading in GHG emission reductions, 6.4 establishes a supervised mechanism like the Kyoto Protocol, and 6.8 recognizes non-market approaches for cooperation without emission reduction trading.