The global conversation around climate change has evolved dramatically over the last decade. Today, the challenge is no longer whether climate action is necessary it is how the world will finance it. From renewable energy projects and electric mobility infrastructure to climate-resilient agriculture and adaptation programs, climate finance has emerged as one of the most powerful enablers of economic transformation. Governments, investors, corporations and development institutions are now mobilizing capital at an unprecedented scale to accelerate the transition toward a low-carbon and climate-resilient future. Yet despite record-breaking investments, the world remains far from where it needs to be.

The question is no longer about the availability of climate finance. The real question is: Who will be able to access it, deploy it effectively and create the next generation of climate-positive growth?

The Rise of Climate Finance: From Billions to Trillions

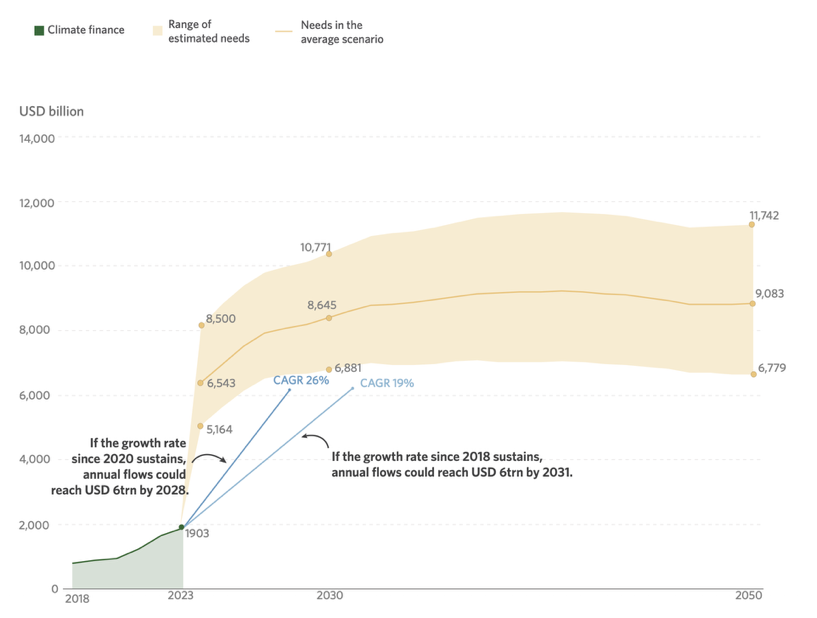

The Climate Policy Initiative (CPI) has reported in its ‘Global Landscape of Climate Finance 2025”that the global climate finance flows have increased from nearly USD 674 billion in 2018 to ~USD 1.9 trillion in 2023 (as shown in Figure), with estimates suggesting that annual investments have already crossed the USD 2 trillion mark. This growth reflects the accelerating momentum in Energy and Transport sectors which are the highest recipients of climate finance, followed by other sectors such as Buildings & Infrastructure, AFOLU, Sustainable buildings, Nature-based solutions and adaptation projects. However, this success story comes with an important caveat.

The report also estimates that achieving global climate goals will require between USD 6 trillion and USD 11.7 trillion annually over the coming decades. In other words, current investment levels while reaching an all-time high still needs to be much higher to keep global warming within manageable limits and build resilience against increasingly severe climate impacts For businesses, governments and investors, this gap represents both a challenge and an opportunity. The organizations that can successfully navigate the climate finance ecosystem will be positioned to unlock significant capital flows and long-term growth opportunities

Why Climate Finance Has Become a Strategic Business Imperative

Historically, climate investments were viewed as compliance-driven expenditures or sustainability initiatives. Today, they are increasingly recognized as drivers of economic competitiveness, industrial growth, energy security and investment returns. Renewable energy, electric mobility, climate-resilient infrastructure and sustainable supply chains are attracting unprecedented levels of capital, reshaping industries and creating new avenues for growth. In markets such as China, clean-energy industries already contribute more than 10% of GDP, demonstrating how climate-focused investments can become powerful economic engines rather than cost centers.

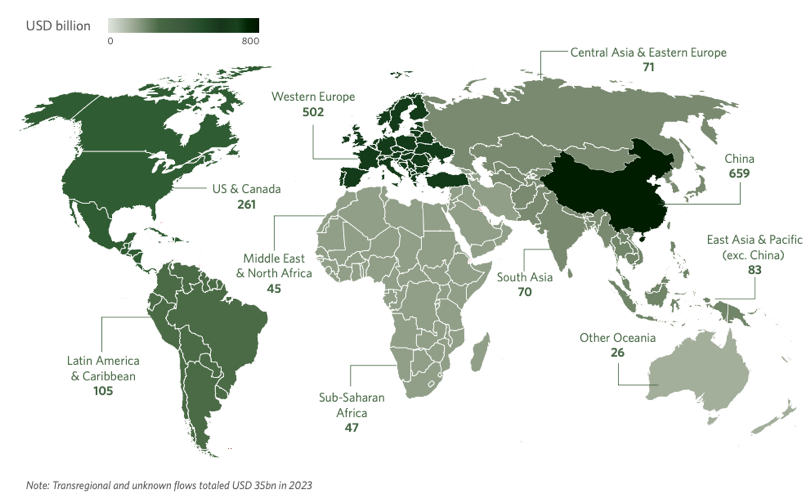

At the same time, climate finance is becoming a key indicator of a region’s ability to attract investment and accelerate industrial transformation. Between 2018 and 2023 as shown in Figure 2, nearly 79% of global climate finance was concentrated in three regions (darker green shade) i) East Asia and the Pacific ii) Western Europe and iii) the United States and Canada highlighting a growing divide between capital-rich and capital-constrained markets. East Asia and the Pacific alone accounted for 39% of global climate finance, driven overwhelmingly by China. On the other hand, countries like Germany, the United States, Brazil and India emerged as the leading climate finance hubs within their respective regions.

Climate finance has evolved into a diversified ecosystem supported by public institutions, multilateral agencies, private investors, and philanthropic organizations. Governments continue to play a foundational role through climate budgets, incentives and dedicated funding programs and multilateral development and regional development banks provide concessional financing, guarantees, and technical assistance to de-risk investments. At the same time, private capital has emerged as the largest source of climate finance, with institutional investors, infrastructure funds, private equity firms and corporations increasingly directing capital toward these technologies.

The climate finance landscape is also being strengthened by a broad range of financial instruments tailored to different project needs and risk profiles. These include grants, concessional loans, green and sustainability-linked bonds, equity investments, risk guarantees, blended finance structures, project level Market rate debts and carbon market mechanisms. Increasingly, these instruments are being combined to enhance project bankability, reduce investment risks and attract larger pools of institutional capital, enabling the scaling of climate and sustainability-focused investments.

Looking Ahead: The Next Decade Will Define the Climate Finance Landscape

The climate finance landscape is entering a period of unprecedented growth, driven by stronger government commitments, expanding climate-focused lending from development finance institutions and increasing participation from institutional investors. At the same time, innovative financing mechanisms and blended capital structures are improving project bankability and accelerating investment flows into low-carbon and climate-resilient sectors. The funding availability continues to expand, organizations that can develop robust climate strategies, build investment-ready projects and effectively navigate the evolving financing ecosystem will be best positioned to unlock new growth opportunities.

pManifold’s Climate Finance Portfolio

pManifold is a leading consulting and advisory firm focused on e-mobility, climate finance, new energy, transport, green hydrogen and carbon markets. Headquartered in Nagpur, India, it has delivered 400+ projects globally, including 200+ e-mobility and 15+ climate finance assignments across developing regions. Its climate financing practice has been developed through sustained engagement with multilateral climate funds, development finance institutions and international donors. Our expertise spans the entire climate finance lifecycle, from concept development and readiness support to fund structuring, financial instrument design and mobilization. Key service areas include:

- Climate Funds Access & Proposal Design: End-to-end support for climate finance access, including concept note development, readiness support, funding proposal preparation and donor engagement

- Techno-Commercial Due Diligence: Evaluation of technologies, business models, market readiness, commercial viability and investment potential of projects and programmes

- Project Structuring & Bankability Support: Design of investment-grade projects, financial frameworks, implementation models and bankability assessments to attract public and private investment

- Blended Finance & Capital Mobilization: Structuring of concessional finance, guarantees, viability gap funding, matching grants and PPP mechanisms to mobilize capital for sustainable development projects

- Modelling of Financing Instruments and Their Impact: Financial modelling and assessment of financing instruments, including analysis of leverage, risk allocation, affordability and climate impact

- Policy & Regulatory Advisory: Analysis and design of policy instruments, incentive mechanisms, pricing frameworks, green taxonomies and regulatory measures to accelerate market development