In Africa itis estimated that stationary battery capacity could grow by 22% annually through 2030 due to demand from energy access applications, and mini grids alone could represent 40% of the 2030 market. Market forecasts by the World Economic Forum show that as more Africans gain access to energy over the coming years, the demand for batteries will grow to 83 GWh by 2030.

While there is a growing demand for batteries in Africa, currently it has very little capacity to produce or recycle batteries and is not as well-established as in other parts of the world. This appears to be a huge opportunity for the continent to take control of its destiny by investing in developing these capabilities and reducing reliance on foreign imports. This has the added benefit of creating local jobs and elevating the continent’s economic productivity. Additionally, battery recycling is also an important way to reduce the environmental impacts of battery production and disposal, as well as to conserve resources.

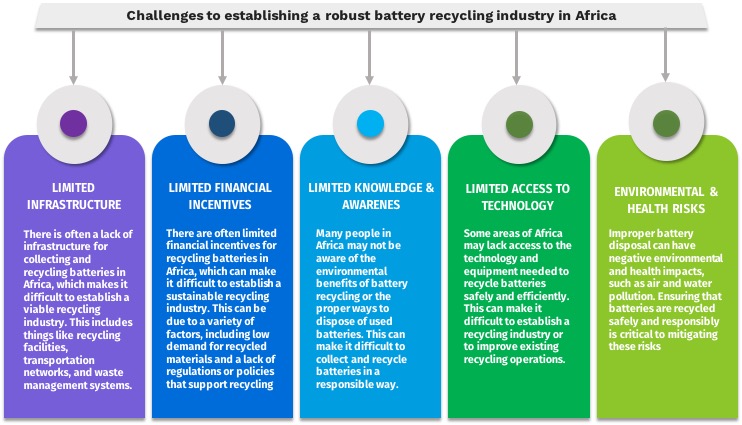

However, there are several challenges to establishing a robust battery recycling industry in Africa. Some of the main challenges include:

Despite these challenges, there are a number of efforts underway to improve battery recycling in Africa. For example, the Africa Battery Alliance is a partnership between the African Union and the International Renewable Energy Agency (IRENA) that aims to accelerate the development of a sustainable battery value chain in Africa. This includes efforts to promote battery recycling as well as to increase the use of renewable energy storage systems.

Other organizations, such as the African Battery Recycling Association, are working to raise awareness about the importance of battery recycling and to establish best practices for battery collection and recycling in Africa.

Overall, while battery recycling in Africa is still in the early stages of development, there are a number of efforts underway to improve the situation and reduce the environmental impacts of battery production and disposal.

Factors influencing future of battery recycling in Africa

One of the key factors that will influence the future of battery recycling in Africa is the increasing demand for batteries in the region. As the adoption of electric vehicles, renewable energy systems, and other battery-powered technologies continues to grow in Africa, there will be a need for more batteries to meet this demand. This could create new opportunities for battery recycling in the region.

Another factor that could influence the battery recycling in Africa is the development of new technologies and business models. As battery technology continues to evolve, it is likely that new approaches to battery recycling will emerge, which could make it more economically viable to collect and refurbish used batteries in Africa.

The future of battery recycling in Africa will also be influenced by regulatory and policy developments. Governments in the region will have a role to play in establishing frameworks and incentives that support the collection, treatment, and recycling of used batteries, and in promoting the use of recycled batteries in various applications (Distributed Renewable Energy(DRE) applications like solar fridges)

All in all, the future of battery recycling in Africa is likely to be shaped by a combination of economic, technological, and regulatory factors. As these factors evolve, it is likely that battery recycle will become an increasingly important aspect of the region’s efforts to manage its e-waste and reduce its environmental impact.

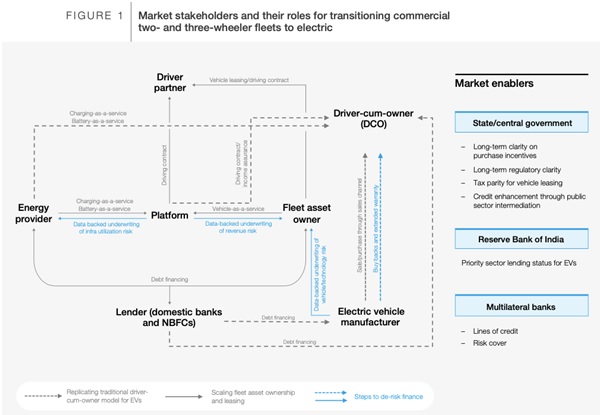

In collaboration with NITI Aayog, the World Economic Forum (WEF) published a report on the financing options in India’s Electric Vehicle (EV) industry. The report highlights capital pools and their lending status in the EV ecosystem, as well as a multi stake holder approach to market de-risking for transitioning two- and three-wheeler fleets to electric.

Two-wheelers (2W) and three-wheelers (3W) account for over 80% of vehicle sales in India.

The adoption of electric 2W (or e-2W) and 3W (or e-3W) has been rising steadily, supported by government policies like Faster Adoption and Manufacturing of Electric Vehicles (FAME), 40+ vehicle manufacturers, others and an impressive cumulative sales of 1 million units has been achieved. However, this is still just 1 million out of India’s total 2W and 3W fleet stock of 250 million – leaving enormous room for continued growth. Achieving 100% electrification of India’s 2W and 3W stock is estimated to require a capital allocation of approximately $285 billion.

Although initial purchase cost of EVs is higher, their running or operational cost is much lower than its counterpart Internal Combustion Engine (ICE) vehicle. Total cost of ownership (TCO) metrics show that they are already ideal for last-mile delivery and ride-hailing fleets, both of which have high daily utilization rates. For instance,

TCO of e-2W is INR 0.52/km (after accounting FAME incentives and specific Delhi fleet scenario) in comparison to its ICE as INR 2/km

The TCO of e-3W is INR 1.94/km in comparison to its ICE as INR 2.25/km for the similar scenario of Delhi fleet and accounting FAME incentives

These markets are pioneering the use of e-2Ws and e-3Ws in India and are probably among the first to make the full switch to electric. The ecosystem needs to see a multi-fold increase in capital flow if fleets are to transition quickly. De-risking the market will require improved stake holder collaboration and business model innovation in order to open large capital pools. The different capital pools and their status in EV lending are listed below and divided into three categories.

Unlocked

Private equity has been the first pool of capital that has been unlocked and in 2021, the sector received USD 1.8 billion investments by OEMs, fleet owners, fleet operators and infrastructure providers

Partially Unlocked

Non-banking Financing Companies (NBFCs) are currently the main source of debt financing in this sector. NBFCs backed by Original Equipment Manufacturers (OEMs) and those specializing in vehicle financing are expected to play a greater role in financing EV fleets.

Dedicated climate funds like Green Climate Fund(GCF) and Global Environment Facility (GEF) Trust Fund have approved a fund of 1.5 million USD and ~172 million USD. Such funds are being channeled through multilateral banks and other implementation partners.

Other capital options that are anticipated to encourage and draw investments in green projects in the nation over the coming years include multilateral banks, venture capital, and green bonds.

Locked

Most domestic banks and international banks with commercial operations in India have largely stayed away from financing electric two- and three-wheeler commercial fleets.

Multi stake holder Approach to Market de-risking

No individual stakeholder can de-risk adoption for e-2W and e-3W fleets. Key stakeholders need to collaboratively engineer and test solutions. Traditionally, the driver-cum-owner (DCO) model has dominated the two- and three-wheeler commercial fleets in India, but DCOs of commercial fleets are not yet comfortable to purchase EVs due to the higher upfront cost of acquisition, lack of confidence in new technology, unassured reliability and unestablished resale value.

Tripartite agreements to spread the risk

To de-risk lending and cost of finance for large fleets, a tri-partite lending agreement between lenders, OEMs and fleet asset owners can spread the risk across parties. OEMs can underwrite technology risk, assure buy-back value and ensure after-sales service. Platforms can issue longer-term contracts to driver-partners, aggregators, etc. for deployment of EVs to underwrite risk of insufficient demand – enabling higher asset utilization for vehicle-as-a-service partners – resulting in consistent revenue stream that allows lenders to underwrite EVs for commercial operations and provide low-cost debt-funding to EV fleets.

Residual value and performance of EVs to be established

Residual value of EVs is not yet established, which increases uncertainty, affects purchasing decisions, and availability and cost of financing. OEMs can set expectations on residual value of used vehicles through buy-back programmes, or battery and product warrantees. Through use of data and analytics, vehicle manufacturers can track usage-based battery and vehicle health and can make that data available for stakeholders involved in resale.

Risk underwriting for lending needs to be able to leverage data

Unlike conventional vehicles, EVs and the supporting charging infrastructure

are in equal part connected devices generating real-time data. These data sets can be leveraged to facilitate data-backed risk underwriting for lending. For example, OEMs can make available anonymous and aggregated data sets on asset utilization and data on health of battery as the vehicle ages. The banks understanding of the technology is limited and provision of these type of insights can introduce competitive financing products.

Support to vehicle leasing vis-à-vis individual ownership

India has among the smallest share of 0.8% of leasing-based commercial fleets among large economies. Even as DCOs acquaint themselves with EV, fleet asset owners that rely on vehicle leasing can drive EV adoption in India’s commercial fleets. Leasing of commercial vehicles for fleets has a higher tax burden as compared to individual ownership – parity in tax structures for EVs can help scale up EVs on the road.

Preferential access to finance is required

It has been a long-standing demand from the industry that the Reserve Bank of India provide priority sector lending (PSL) status to EVs, on the lines of PSL for renewable energy projects to help channel flow of funds to the sector. Priority sector lending mandates certain banks to direct a specified percentage of credit to priority sectors.

Government push for setting up of risk-sharing facilities for consumer and fleet finance

To accelerate the market and steepen the learning curve for lenders, the government can work with multilateral banks and/or deploy its own special purpose vehicle (SPV) to provide sufficient first-loss risk guarantee to lenders. SIDBI-World Bank Electric Vehicles – Risk Sharing Program (EV- RSP) is an example of this.

More details can be referred from the following link:

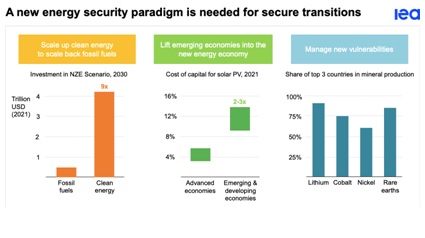

The International Energy Agency (IEA) recently published a report on the global energy outlook as part of its World Energy Outlook 2022.The report highlights the global energy crisis, which has been triggered by the conflict in Ukraine, and has resulted in significant price increases due to uncertainties about supply security and affordability. This comes at a time when energy markets are already tight following the COVID-19 rebound.

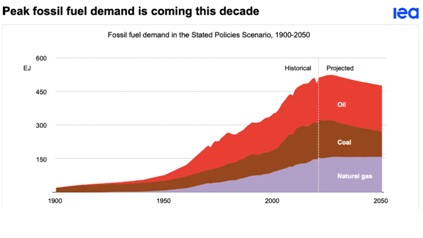

According to their “States Policies Scenario, 1900 – 2050,” the global demand for all fossil fuels is now exhibiting a peak or plateau for the first time.

In this scenario, coal use declines over the following few years, natural gas demand reaches a plateau by the end of the decade, and oil demand gradually declines through the middle of mid-2030s due to rising sales of electric vehicles (EVs). This indicates that from the mid-2020s to 2050, the global demand for fossil fuels will gradually decline. As a result, the proportion of fossil fuels in the global energy mix will fall from around 80% to just above 60% by 2050. Global CO2 emissions will gradually decline from a high of 37 billion tonnes per year in 2010 to 32 billion tonnes by 2050.This would be associated with a rise of around 2.5°C in global average temperatures by 2100, far from enough to avoid severe climate change impacts.

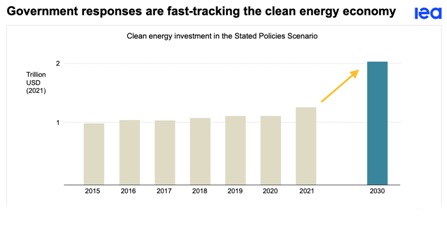

To minimize the impacts of the energy crisis, advanced and emerging economies/governments are now taking historic and decisive steps toward a cleaner, more affordable, and more secure energy system. Some of the most notable ones are “The US Inflation Reduction Act”, “the EU’s Fit for 55 package”, “REPowerEU”, “Japan’s Green Transformation (GX) programme”, “Korea’s goal to increase the share of nuclear and renewables in its energy mix”, and “ambitious clean energy targets in China and India”. These new

measures help propel global clean energy investment to more than USD 2 trillion a year by 2030, a rise of more than 50% from today in the States Policies Scenario. While clean energy investment rises above USD 2 trillion by 2030 in the States Policies Scenario, it would need to be above USD 4 trillion by the same date in the Net Zero Emissions by 2050 Scenario, highlighting the need to attract new investors to the energy sector. And major international efforts are still urgently required to narrow the worrying divide in clean energy investment levels between advanced economies and emerging and developing economies.

Amid the major changes taking place, a new energy security paradigm is needed to ensure reliability and affordability while reducing emissions. In this transition, declining fossil fuel and expanding clean energy systems will co-exist, since both systems are required to function well during energy transitions in order to deliver the energy services needed by consumers. And as the world moves on from today’s energy crisis, it needs to avoid new vulnerabilities arising from high and volatile critical mineral prices or highly concentrated clean energy supply chains.

More details can be referred from the following link:

Electric Vehicles (EVs) are fundamentally 5-6 times more efficient than Internal Combustion Engines (ICEs) because they convert energy directly into motion, as opposed to ICEs, which must first burn fuel to produce heat before converting that heat into motion. Furthermore, the use of EVs and charging stations is expected to increase overall energy efficiency in the transportation sector while reducing fossil fuel use and improving energy security. EVs have a high potential for reducing greenhouse gas emissions because increasing energy efficiency reduces GHG emissions significantly. Many countries have pledged to reduce their GHG emissions[1] by adopting EVs in a variety of vehicle categories. But are all EV segments green? A thorough examination of each variable reveals that they are, butthe answer is nuanced and includes asterisks.

It is highly debatable whether all EV segments are environmentally friendly, owing to the reliance on the electrical source used to charge the vehicle. EVs, for example, are easily justifiable in countries where the majority of electricity is generated using cleaner, fossil-fuel-free technologies (such as nuclear and hydroelectricity).

Power generation in European countries has recently shifted its emphasis to greener technology. The majority of energy produced in developing countries such as China and India, on the other hand, is produced using coal, and as a result of their rapidly expanding economies, they have grown to play a significant role in global CO2 emissions. To better understand the eventual reduction of GHG emissions from various EV categories, it is necessary to investigate their implementation in developing countries. Because increasing the number of EVs without first assessing their GHG emissions could have a negative impact on climate mitigation efforts.

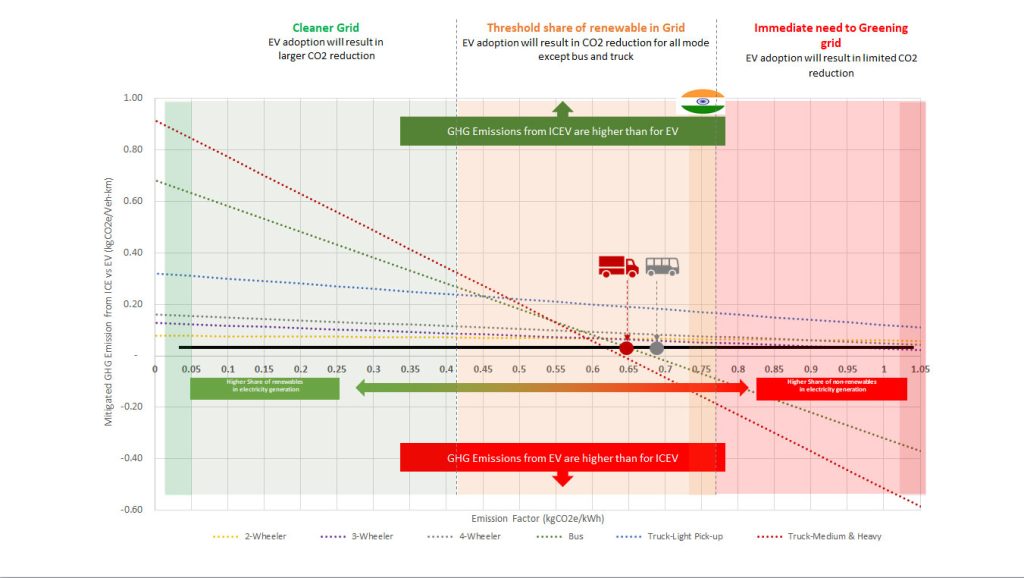

Vehicle emissions are produced during the production process (manufacturing), while the vehicle is being driven (in-use), and after it has finished its useful life. Only in-use emissions will be covered in this article; later articles will go into greater detail about lifecycle emission assessments. As indicated in the figure below, mitigation of GHG emissions from ICE vs. EV is done nationwide using all grid parameters.

A nation’s grid factor is a crucial metric to consider when evaluating emissions across various EV segments (GHG emission per unit of electricity production). Higher grid factors are associated with greater non-renewable energy use in a nation, and vice versa (as plotted on x-axis of diagram below).

In the case of India, with a grid factor of 0.75, the GHG mitigation potential is positive for all EV segments except buses and trucks as shown in the figure.

[1] GHGs included under UNFCCC are carbon dioxide (CO2), methane, nitrous oxides, perfluorocarbons, hydrofluorocarbons, sulfur hexafluoride, and trifluoride nitrogen. Only CO2, methane, and nitrous oxide are relevant to the transport sector. However, according to UNFCCC methodologies for determining emissions from the transport sector, nitrous oxide emissions are very marginal. Therefore, only CO2 emissions are included and, in addition for gaseous fuel-powered engines, emissions of methane

* kgCO2e/Veh-Km: kilogram of carbon dioxide equivalent emission per Vehicle kilometre travelled * kgCO2e/kWh: kilogram of carbon dioxide equivalent emission per kilowatt-hour * ICEV: Internal combustion engine vehicle*EV: Electric vehicle *Fuel efficiency of ICE vehicle segment: 2Wheeeler – 25 kms/litre; 3-Wheeler – 25 kms/litre; 4-Wheeler – 20 kms/litre; Bus – 5 kms/litre; Truck Light pick-up – 10 kms/litre; Truck-Medium & Heavy – 4kms/litre *Fuel efficiency of EV segment: 2Wheeeler – 52 kms/kWh; 3-Wheeler – 10 kms/kWh; 4-Wheeler – 9 kms/kWh; Bus – 1 kms/kWh; Truck Light pick-up – 5 kms/kWh; Truck-Medium & Heavy – 0.7 kms/kWh *Only In-use vehicle emissions has been accounted

Source: pManifold Analysis

It should also be noted that in countries with a grid factor greater than 0.8 kgCO2e/kWh, decarbonizing the grid should be the top priority. Because the impact of EVs on GHG reduction in such countries will be small, with high marginal abatement costs. According to experts, starting with EVs and decarbonizing the grid in parallel to promote EVs is not an effective strategy because grid decarbonization, in general, takes a long time due to the long life span of energy production units.“EVs are green for most of the vehicle segments except bus and medium & heavy-duty truck in terms of in-use GHG emissions”

Asian countries with a high share of renewable electricity production, such as Armenia, Bhutan, Georgia, the Kyrgyz Republic, the Lao People’s Democratic Republic, Nepal, and Tajikistan, will see the greatest CO2 reductions from EV deployment, whereas India, Indonesia, Kazakhstan, Mongolia, and Turkmenistan will see limited CO2 reductions.[1]

Thus, it is discovered that EVs are green in terms of in-use GHG emissions for the vast majority of vehicle segments, with the exception of buses and medium and heavy-duty trucks[2], even when the electric grid is heavily reliant on fossil fuels.

[1] Country-wise list of Grid emission factors is given by IGES

[2] Bus and medium & heavy-duty truck will result in significant GHG reductions if the grid factor is below 0.7 kgCO2e/kWh

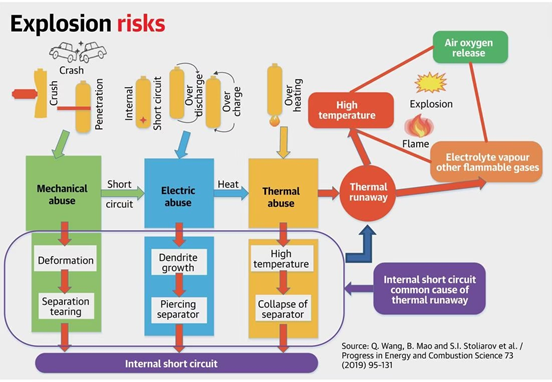

Recent incidents of fires in electric vehicles – two-wheelers ( e-2w) in particular – have brought focus on the safety of electric vehicles. These incidents have put a dent in the growth of EV market, which needs to be urgently addressed.

Causes of fire in EVs

The sources of fire are varied. While most of the fires originate from the battery (thermal runaway), some of the other causes have also been found such as short circuits and glitches in regenerative braking. There are multiple cells in a battery pack, each loading and ageing slightly differently, which may cause what are called ‘hot-spots’ at specific locations in the pack. The charging-discharging cycles can result in abnormally high accumulation of heat at these hot-spots, leading to rising temperatures. However, a battery engineer of a leading e-2W, says that despite the reality of climate change and that summers are getting hotter, an EV battery made up of lithium-ion (Li-ion) cells requires a temperature rise of more than a100 °C before getting into thermal runaway and leading to fires.

While hot weather conditions and inadequate thermal management systems of the battery can negatively impact performance and shorten life, they do not necessarily cause fires. Manufacturers of most modern Li-ion batteries ensure that they automatically switch off battery operations around 45-55 °C of battery temperature. Even if these safety features aren’t built-in, it’s impossible for the ambient heat and the heat generated by batteries together to result in a spike of over a100 °C.

Preventing fire events with good battery design and protection system

Automotive Industry Standard (AIS) drafted by ARAI address the testing and certification of vehicles and engines used for both automotive and applications. They play an important role in ensuring safer, less polluting, more efficient, and more reliable vehicles.

The standard AIS048 deals with mandatory for battery compliance testing. This was originally used for lead-acid batteries but has been upgraded since for Lithium Ion batteries as well.

There is also a need to have a good battery design to prevent such fire incidents. Cylindrical Lithium-Ion (Li-Ion) cells are a good choice for EVs, which has two internal protective devices: the Positive Temperature Coefficient (PTC) and the Current Interrupt Device (CID) . The PTC protects the cells under external short conditions and the CID protects the cells under overcharge conditions. The casing of the battery should be heat conductive, robust in structure, and have electromagnetic interference (EMI) shielding. The need for effective EMI shielding is especially prevalent in electric vehicles to minimize the associated risks like damage of electrical and electronic components from corrosion, heat, and other challenging conditions.

In the case of an external short circuit, several layers of protection are required such as Battery Management System(BMS) preventive & diagnostic functions, pack fuse, and CID. Batteries also have some sensitive components like MOSFETs, and current resistors that need to be protected. Also, temperature sensors are required to monitor the battery temperatures and alert the user about possible fire risk. Therefore, industry and manufacturers need to spend sufficient time integrating safety features, testing and verifying their products to avoid such accidents in the future.

Regulatory requirements

The Global Technical Regulations are developed under the International Agreement on Vehicle Construction, to which the EU is a Contracting Party. This Agreement currently has 38 Contracting Parties (including the EU, Japan, Russia, Korea, China, India, and the United States of America). The Regulations cover the approval of vehicles’ safety and environmental aspects and are managed by the World Forum for Harmonization of Vehicle Regulations, a permanent working party of the United Nations Economic Commission for Europe (UNECE). In India, The Automotive Industry Standard has over 40 standards published that cover safety from the level of individual components. That testing is concerned with electric vehicle battery safety and lays out requirements of how those batteries must be able to tolerate a wide spectrum of abuse.

Currently, there are AIS156 in-line regulations with AIS136 for the design of electric vehicles and global technical regulations for automobiles and buses. The EVSGTR20 is designed for Phase I of this regulation, which has already been published, and Phase II focuses on electric two-wheelers. Regulations on passenger cars and buses AIS038 (Revision 2) are aligned to EVSGTR20. Regulations have been updated in all other countries in accordance with GTR20.

AIS Standards for Electric Vehicles and Chargers

Standards

Description

AIS-038 – Electric Power Train Vehicles-Construction and Functional Safety Requirements

It includes requirements of a vehicle with regards to specific requirements for the electric power train and requirements of a vehicle Rechargeable Electrical Energy Storage System concerning its safety.

AIS-039 – Electric Power Train Vehicles–Measurement of Electrical Energy Consumption

It helps in measuring the consumption of electric energy by electric vehicles

AIS-040 – Electric Power Train Vehicles – Method of Measuring the Range.

It is a range test for the electric vehicles

AIS-041 – Electric Power Train Vehicles – Measurement of Net Power and The Maximum 30 Minute Power.

It helps in the measurement of the net power of the electric vehicle and explains the working and benefits of the maximum 30-minute power.

AIS-049 – Electric Power Train Vehicles – CMVR Type Approval for Electric Power Train Vehicles.

It is a test of grade-ability for electric vehicles.

As per Deputy Director, ARAI, fire incident is a quality issue against the default because after all, you don’t see every EV battery catching fire, but only a few of them. Therefore, instead of calling on the government to regulate, OEMs need to self-regulate.

India is participating in Phase II of the GTR20, which focuses on heat transfer, water immersion, safety requirements, and more for two-wheeler batteries. For the two-wheeler, the AIS156 was intended for mechanical abuse, thermal abuse, and electrical abuse. Apart from certification and testing, manufacturers need to perform proper design, internal testing, verification beyond certification testing, manufacturing processes, and even pattern recognition charging and discharging.

Ways to extinguish Fire

When the battery is fired, it reaches a temperature of 70°- 90°C. This is shown in various test results. There are many ways to extinguish a fire. There are three ways to put out the fire.

Lower the temperature

Separate oxygen from fire

Remove flammable material

Water cooling is the best method due to its large specific heat capacity (i.e., 4.2kJ/kg°C), it can absorb a significant amount of heat and reduce its temperature. Water also covers the surface of flammable substances, so it can also separate oxygen from the fire.

What can customers do?

Avoid charging the battery immediately after stopping the EV from running. The lithium-ion cell contained in the battery remains hot for some time. Allow the battery to cool before charging.

Use only vehicle-specific batteries and charging cables. Using cheaper local batteries can damage your mobility device.

If the battery is removable, do not place it in direct sunlight or in a hot vehicle. Also, protects the vehicle and battery from extreme temperatures. Batteries and chargers should be stored in a clean, dry, and well-ventilated place. Do not drain or fully charge the battery. Essentially, they should be between 20 – 80%

Regularly check the battery for damage before use, discontinue use and report to the manufacturer if any are defective. Do not use if the battery is extremely hot or damaged

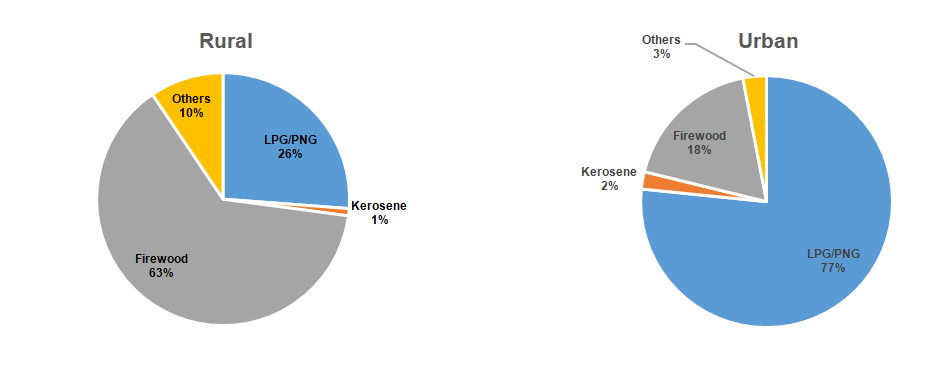

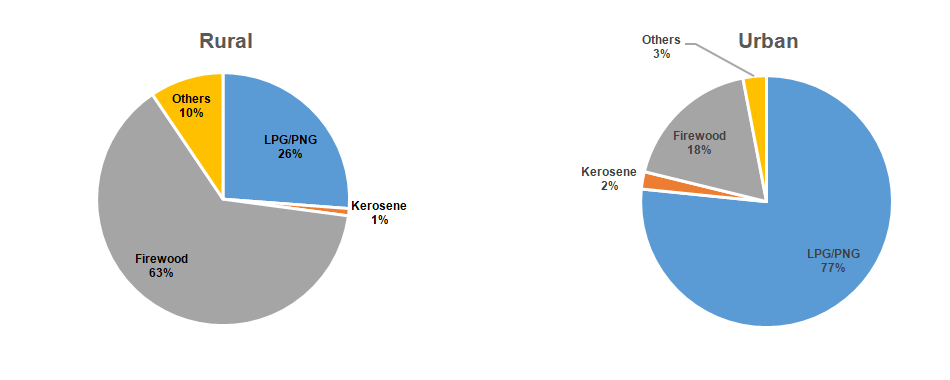

Approximately 40% (2.8 billion people) of the global population still cooks with either wood, dung, coal, or charcoal. Nearly 84% of rural Indian households cook on stoves that use solid or biomass fuels. In India, women spend an hour every day collecting firewood. This time dedicated to collecting firewood and cooking limits their ability to attend school and generate income. Moreover, women are exposed to toxic pollutants released from the burning of solid fuels (wood, charcoal, etc.).

Also, the burning of solid fuel in inefficient traditional stoves is responsible for the emission of various indoor air pollutants, which have direct and indirect impacts on the health of women and children. According to the Global Burden of Disease estimation, solid fuel burning for cooking accounted for 6 lakh premature deaths in 2019 in India. Thus, it is need of the hour to transition to electric cooking solutions which include access to electricity, and cleaner, more efficient stoves.

Benefits of Electric Cooking

Electric cooking is cost-effective, safer, more energy-efficient, requires less maintenance than conventional cooking methods, and is free of emissions. Additionally, Electric cooking can also make use of solar power in both urban and rural areas. Presently, about 24% of the electricity consumed in India is generated from renewable resources, and planning to expand it to 40% by 2030. This will be more viable in rural areas where the electricity grid may not be very reliable but solar energy is easier to provide.

Some of the key benefits of electric cooking are:

1

Speed – Cooks food 50% faster

2

Energy efficiency – savings in energy consumption and reduction energy usage cost

3

Easy & Precise Control – Achieve desired temperature

4

Safety – No flame, no gas leakage

5

Low maintenance –Change of burners, pipe, and regulators on periodic basis not required

6

Compact – Can be easily transferred from one place to another

7

Improves health – Prolonged exposure to smoke arising from conventional indoor cooking methods adversely impacting health

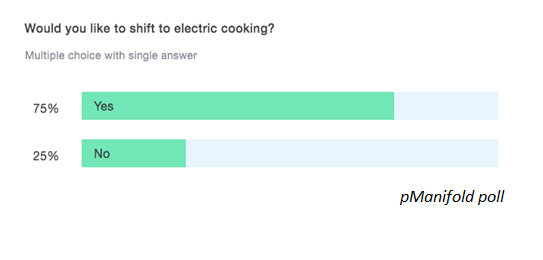

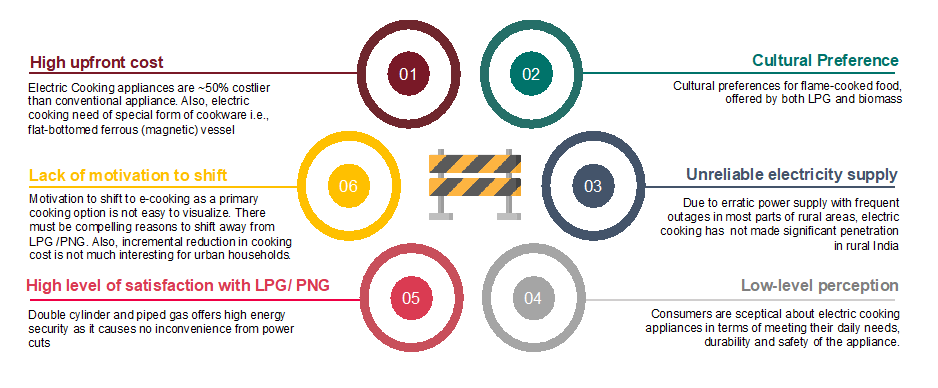

Despite the benefits of electric cooking only ~5% households use electric cooking devices today.

Moreover, there is a high willingness to shift to electric cooking, however, there are certain barriers which needs to be addressed. Let’s understand what are these barriers!

Barriers to transition to Electric cooking

Getting consumers to adapt to new technology is a tricky proposition anywhere, but when it comes to electric cooking, its adoption remains riddled with more challenges. Affordability remains the topmost one, especially for a household that relies on biomass fuel which is available for free. An electric cook stove (induction to be precise)uses electromagnetism to heat cookware, which means that the utensils have to contain enough iron to generate a magnetic field around them. For a consumer, this not only means bearing upfront costs, as well as maintenance costs, but also the cost of switching to compatible cookware. This is something the majority of the households might not be willing to bear when their existing utensils and source of fuel are working to their convenience.90% of Ujjwala beneficiaries still use solid fuel for cooking.

The flame-based cooking offered by LPG and biomass is an important barrier that needs attention and resolution as chapatis, an integral food item of an Indian meal does not get cooked properly on an electric cookstove. According to a survey conducted by the Stockholm Environment Institute, majority of Indian women surveyed in rural area said they preferred cooking chapatis the traditional way in a clay oven, or over open fire, because it tastes better.

Another critical barrier is thelow-level perception for electric cooking mostly in rural areas. This issue is especially important, because it is this that is at the heart of the successful adoption of electric cooking technology. Consumers are sceptical about electric cooking appliances in terms of meeting their daily needs, durability and safety. Even though, firewood and LPG based cooking is quite unsafe.

In urban areas, there is lack of motivation to use electric cooking appliance. The incremental reduction in cooking cost is not of much interest as there is a high level of satisfaction and security in using LPG/ PNG.

The government of India has made efforts to enhance access to clean cooking energy through the ‘Go Electric’ campaign, launched by the Bureau of Energy Efficiency (BEE) talks about spreading awareness of the benefits of electric cooking in India. The draft National Energy Policy by NITI Aayog also aims to achieve access to clean cooking energy for all by 2022, emphasizing on electric-based cooking. However, this impetus from the government for widespread penetration and adoption of electric cooking is still limited. There is an elemental issue to the government’s plan of powering India’s cooking through electricity which is lack of electricity supply. While huge strides have been made in the area, power supply in most rural areas remains irregular at best. According to news reports, 10 states receive less than 20 hours of power, with nearly 30 million households that don’t receive power. Which brings us to the question — how can electric cooking be adopted if people can’t use it?

Way forward

To help adoption of electric cooking appliances it is important that traditional practices around cooking is understood and either accepted or countered when introducing electric cooking. The value proposition of electric cooking needs to be rightly communicated which requires focused and customized marketing strategies for electric cooking appliances. The varying acceptance patterns for electric cooking by men and women need to be understood and used for targeted communication. Hence, there is a need to build awareness about electric cooking which is not linked to only product features. There is a need for electric cooking industry to invest in social and behavioral research and use the information for product design, diversification and variety and also for marketing communication drive the transition.

Moreover, the potential end-users needs to be correctly identified. Pushing the economically stressed rural households with intermittent power supply may not be the right stakeholders for to start electric cooking uptake. If it has to then it needs to be supported by right financing mechanism. Rather it could be the urban population (including hotels, hospital, office canteens, schools and other institutions) with stable electricity supply that can be targeted for mass adoption. Possibly India may not transition completely to electric based cooking but both forms can co-exist with electric becoming the primary source of cooking. Moreover, if the Government of India develops a dedicated program to promote electric cooking with the participation of all State Governments, electric utilities, and all other related stakeholders and civil society associations to an aim to make electric cooking affordable and user-friendly for lower strata of the society, then electric cooking definitely will see a brighter future.

Globally climate change is causing catastrophe damage to natural environment deterring the economic progress. Increase in global population, rapid urbanization has caused a huge surge in transport demand resulting in rise of transport emissions.The transport sector is prime contributor to greenhouse gas emissions (GHG) responsible for 24% of carbon dioxide (CO2) emissions with surface transport accounting for nearly three-quarters of transport CO2 emissions. Decarbonization is the vital component that helps attenuate climate change by restricting CO2 emissions.This calls for rapid decarbonizing strategies to achieve net zero emissions as outlined in the Paris Agreement.The governments worldwide are eyeing development plans leading to low GHG emissions and boosting the social, economic, and environmental growth thus paving way for low emission development strategies (LEDS).

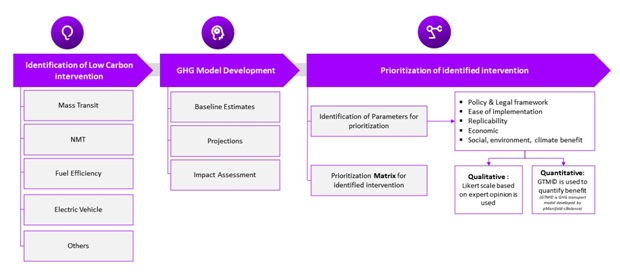

How LEDS can help achieve low carbon economy?

LEDS provide integrated planning to advance national economic development and climate change policies in a more integrated, systematic, and strategic way.It can be designed to create a holistic intervention plan by identifying low carbon transport interventions which can be emission standards, shared mobility, electric passenger vehicles, improvement of fuel efficiency, etc. GHG modeling can be developed for baseline estimates, projection and impact assessment of each identified intervention. A prioritization matrix can be developed based on different criteria like Policy and Legal Framework, Ease of Implementation, Economics, Social Benefits, Environment Benefits, Climate Benefits and Replicability. Marginal Abatement Cost Curve (MACC) analysis which is one of the key parameters can be done to quantify benefits and prioritize the interventions based on abatement cost.Targets can be defined for each identified intervention to make improved policy decisions.The entire process of prioritization can be done in collaboration with stakeholders. An institutional structure can be proposed for interventions which ensure smooth policy and planning regulation, its execution and monitoring and control. Also, action plans to identify most suitable sources of financing options available for each LEDS intervention can be explored.Thus, LEDS can help achieve low carbon economy.

The proposed LEDS can be a standard setting instrument that helps identify the source of GHG emissions of a country and provides staggering data from prioritization of interventions. It can result in strong collaboration of development planning and scientific analysis. It can enhance framework conditions necessary for private sector investment in mitigation actions. Thereby helping the countries to achieve zero emission. Such strategic planning and analysis have been carried out by pManifold for one of its client country.All in all, low carbon emissions can be accomplished with strategic planning and timely actions.

India stands strong in achieving universal access to electricity with almost 100% electrification by 2019. The national grid has played a very important role in improving this access, but its reliability continues to pose a challenge, and more so in semi-urban, rural and remote areas. Distributed Renewable Energy (DRE) in the form of solar roof tops (SRT) and solar home systems (SHS) tied with efficient appliances help improve reliability of service and are seeing increased adoption. By some estimates, there are approximately 4 million HHs (1.4% of the total 277 million HHs in India) with some form of SRTs or SHSs in India.

Many of the previously used SHSs were standalone systems powering AC and/or DC Appliances with energy storage. Today, there is a new class of DRE solutions commonly termed Hybrid Solar Systems, which integrates solar with AC grid power (uni or bi-directional) and can power AC and/or DC appliances. Such new Hybrid AC-DC (HAD) power solutions can help users to take advantage of solar power – improving supply hours and reducing their Power Distribution Company (Discom) energy bills. India saw estimated annual sales of some 0.8 million units of solar hybrid inverters or uninterruptible power supply (UPS) systems in 2019 (compared to some 8 million-unit sales of conventional inverters) and there is an expected increasing trend.

More and more power systems and appliances OEMs and System Integrators are joining this fast-growing HAD market in India. There is a new class of efficient appliances (including lights, bulbs, fans, TVs, refrigerators, washing machines, pumps, etc.) that use fundamental DC-run LED or BLDC motors, and can be run on AC supply and/or DC supply. Some further innovations in appliances include embedding energy storage inside the appliance to avoid the need for costly centralized power back-up solutions. These innovations on the appliances side will further push for increased need of enabling HAD infrastructure for the synergistic co-existence of AC and DC.

In this regard GOGLA initiated a whitepaper which evaluated the opportunities for HAD infrastructure in India. The paper evaluates potential customer segments expected to drive the demand for HAD solutions. The demand assessment identified HHs with no power back-up solution, potential HHs with grid-connected solar rooftops, existing conventional inverter customers, existing mini/micro grid customers and existing SHS users as the potential customer segments to transition hybrid solar systems.This paper also suggests three key strategies to enable these customer segments HHs to shift to HAD power solutions as below:

Strategy-1: Upgrading existing power back-up solutions

Strategy-2: Adding new HH that do not have any power back-up solution

Strategy-3: Replacement at end of product life

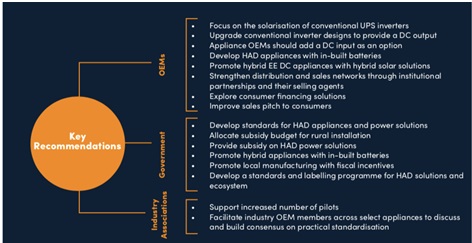

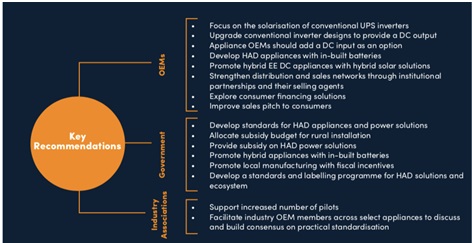

To further strengthen the HAD infrastructure in India, below key recommendations were made to the OEMs, Government and Industry Associations. The findings of the study were shared through an online webinar along with industry experts.

During the launch event, Padmashri Prof. Ashok Jhunjhunwala stated small (<1kW) and large (>3kW) size of HAD power solutionwhich can also feed solar power back to grid can be designed at low-cost and scaled-up. It has immense potential to cover every home in India. He also emphasized that there is a need for remote monitoring, data analytics and controls to designsuch HAD system which will ensure there is no wastage of solar power, minimum usage of AC grid power and at the same time have sufficient power back-up.

Shiva Srivastava, Marketing Leader Asia from Greenlight Planet converged on the thoughtthat HAD is a very promising technology and futuristic as lot of homes are getting connected to grid and already using SHS. Venkat Rajaraman, Chairperson GOGLA India Working Group highlighted the strong need of hybrid AC-DC infrastructure as there is proliferation of EE DC appliances and grid extension. He also mentioned that he views HAD technology for residential sector would fit well and also be a big opportunity area for HAD power solutions.

Rajesh Kunnath, Radiostudio and Convener IEEE LVDC Standards said there are many gaps in standards and there has to be reports like this which act as a backbone to understand HAD architecture and credible market opportunity that is scalable. This will energize the standards body and pave way for manufacturers to participate in standardization to improve reliability. Adding to this Makena Ireri, Manager from CLASP highlighted that it will be important to facilitate R&D and pilot demonstrations as they help bringing more market players and bringing down the technology costs.

Acknowledging the study, Koen Peters, Executive Director, GOGLA mentioned that the research has come very timely as there are developments in industry with EE DC appliances and hybrid solar systems. He also stated that standardization may be a driver to innovation, and it would be wise for the industry to come up with the ideas as to what needs to be standardized and in what ways, before bringing it to BIS or IEEE to have a better direction to promote innovations.

It was concluded by Rahul Bagdia, Managing Director, pManifold that evidently the market is heading towards hybridization, i.e. integration of AC-DC power supply and appliances that support these systems. However, challenges like high upfront equipment cost, high sales effort, low customer awareness, and lack of standardization are an acknowledged reality. Yet, these factors should not deter off-grid players from diversifying and offering HAD solutions to customers. The key industry stakeholders like OEMs, Government and Industry Associations will play a vital role towards mitigating these challenges and enabling growth of HAD infrastructure in India.

Utilities are heavily driven by outsourcing of products and services, but most times, their integration is limited by lack of strong Service Level Agreements (SLAs) and vendor management practices. The new private operators usually start dealing with several products and contractors, and already scarce Management bandwidth gets occupied in monitoring and renegotiating contracts and performance. The key question here is – can organized vendors be developed with more end-to-end managed services for these new PPPs?

Recently, pManifold team spoke with Mr. Gagan Aggarwal, MD, Creative Entrepreneurs (CE). The company has 30+ years of experience in providing Turnkey EPC and O&M services for Power and Water utilities. The interview focuses upon ‘What new business models need to emerge for such managed services that have performance-linked contracts?’ The below shared are the author’s personal views and not to be associated with any of his company’s and other associations.

Q1) What differences you have experienced while supporting Power DFs and Discoms with normal scope of contracted work?

In case of Govt. Discoms, the structuring of contracts is more stereotyped. Moreover with union issues, there is also a limitation in terms of certain activities which stand reserved for the staff on rolls of the Discoms. Whereas in case of DFs, there is no such baggage and they are able to formulate contracts much more freely. Also, there is a concerted thrust by these newly formed DFs to enforce strict statutory compliances by their vendors.

The conventional contracts given by Govt. Discoms have predefined and fixed boundaries in terms of role, responsibility & scope, while in case of Power DFs, things are much more flexible. It happens such that we initiate the contract for one specific given activity, but as the scenario keeps changing rapidly, there is an opportunity of augmentation in other types of activities. Based on the circumstances, there are new situations to dealt and attend it, without any loss of time, to make an overall effective contribution.

There has been a very dynamic way of working, while supporting & dealing with Private Power DFs, compared to the conventional contracts offered by the Govt. Discoms.

Q2) How have you tailored and expanded your service offerings and delivery to fit Franchisee model better? What more your current tacit knowledge allows you to do better than others, something like Transformer Mgmt., Meter theft mgmt. etc.?

As we are gaining more experience and that too across various diverse areas, we are able to offer increasingly effective solutions in sync with the requirements of the Franchisees.

In another instance while working in a particular city, it was observed that power theft turned out to be a much bigger daemon & much more difficult to tackle than had been anticipated earlier. Special measures had to be immediately taken up to handle the developing situation so that the project could proceed as scheduled.

Though most activities that we carry have elements of Distribution Network, new subsets keep emerging all the time, mainly due to public reaction and observed deviations from the anticipated results. Like for one of the DFs, we started with the activity of laying their 33KV cables to augment the power availability from the SEB, soon the priority changed to converting the LT Overhead network to Underground to reduce theft and even this job was very dynamic based on the feedback and calculations of energy saving for given Distribution Transformer. Thereafter, only those DTs were taken up which would provide maximum benefit for the cost incurred. So all in all because of the constant challenges faced by the DFs the approach had to commensurate with the situation.

Q3) What changes you went through from moving from normal ‘Contractor’ to specialised ‘O&M Managed services provider’?

Many times the overall cost has been drastically reduced by the implementation of Trenchless Technology in lieu of Trenching methods thereby avoiding the exorbitant restoration charge by the municipal authorities. With the adaptation of appropriate technique suiting the specific site conditions in the urban areas and the quantity based pricing model provides a win-win situation for both the DFs and the service provider. This gives the DF an opportunity to deal with less vendors and for the vendor it becomes a case of economy of scale. It’s given infrastructure in a particular city being able to generate more business.

While normal contract working is more mechanical in its approach, a specialized O&M Managed service provider has to be much more proactive and of a system-study-&-implement kind of outfit. One has to understand the issues, rather than the ‘apparent’ requirements; to do a fair assessment and analysis; to suggest and discuss with the DFs, followed by implementation of the solution, as deemed relevant.

Q4) What loss reduction opportunities you see on both Technical and Commercial loss reduction with integrated O&M services contract?

Lot of integration is possible, if the service contracts are formulated for a phased manner implementation, for instance we do the network study and analysis to suggest the loss reduction schemes in phase I, thereafter we implement the approved schemes by carrying out field execution, then comes the maintenance of the Network.

On the power theft issue, there has to be a strong & clear political will. States where the government & administration has actively supported the efforts to curb the menace of power theft have done subsequently well. Losses have come down, the speed & extent of modernization has gone up, overall power reliability & availability has improved. On the other hand states where authorities have shied away from their role & responsibility in dealing in a stern manner on the power theft issue are languishing at the bottom of achievement charts.

On the technical front, we have to keep exploring and invest in the latest technologies to accurately identify components / areas, which are a source of high percentage losses. which needs immediate attention, so as to provide us with a working life line.

I am of the firm view that, with most cities the power distribution situation is unsustainable, unless we are able to bring down both the technical & commercial losses to an absolute minimum. Energy saved this way is twice as good as energy produced, as the energy produced would again be subjected to such high AT&C losses.

Q5) There is always ongoing tussle for quality and pricing between contractors and Utility Operators. What best practices you have seen in contract design and Monitoring? What new performance linked contracts will you be open to work?

The concept of performance linked contracts is a novel one, but is marred with lot of uncertainties. We are open to such contracts with a rather long term commitment, as only then can there be viability in such contracts.

So having prescribed the minimum must have quality parameters based on the aforesaid attributes, cost should be worked out. And then there is cost associated with a quality work

Yes, this is a classic dilemma, not just in our Industry, but I think its universal. Although such a tussle is an essential ingredient in any system, I would say, we have to go with a balanced approach. We have to go a step further & assign different attributes to quality in terms of minimum quality parameters for safety; minimum quality parameters for statutory compliances; minimum quality norms for long life of the Distribution Network Components etc.

Q6) Managing Labor work force has always been challenging, and so different models of outsourcing and pay roll management emerging with mixed results. How are you tackling this and keeping your grounds team motivated?

Needless to say that an efficient & effective workforce is more than half the battle won, it is very important to have them motivated by incentivizing their working. The incentives have to be assessed based on a very precise monitoring & recognition system. The genuine effort has to be recognized and appreciated. Create similar independent groups capable of carrying a given set of activities, assign similar works to these different groups, induce a healthy competition, the group working more or faster earning better incentives. And provide everyone with the right resources and working environment are some of the practices regularly used at CE.

We have been in this sector for the last 3 decades & have seen a huge change in the availability of labor force. With so many opportunities for them, thanks to the ongoing developmental phase in the country & due to government schemes like NREGA, this resource has become scarce and as a result very precious.

Q7) With your experiences with multiple DFs, how confident you feel that DF could emerge as successful model?

Well very frankly the confidence right now is not very high. The DF models are still evolving, fine tuning the various terms, experimenting with different methodologies. The overall financial scene also makes the current situation give a bleak outlook.

But having said so, I am absolutely clear that there is no option but to sort these issues out. To have any sort of sustenance in the Distribution System across the entire country, the inefficiencies have to be reduced. It may take a few iterations for the best & most effective models/mechanisms to evolve, but they have to eventually evolve.

Since Power features in the basic infrastructure elements of any country, no one can afford to neglect it even in the slightest way. It is so very essential for the nation building that all the stakeholders will have to come together & join hands to take things to the next level.

Distribution Franchisee (DF) model has only recently picked traction since 2009 after successful demonstration by Torrent Power Ltd. at Bhiwandi, Maharashtra, which got operational in 2007. The success there has sparked private businesses interest into the sector with more than 30 corporates jumping into the fray.

Many of the businesses comes from very diverse background of telecom, IT, infra, media, iron & steel etc. and it will be there new entry into the power sector, starting with distribution.

The emerging nature of the DF model, high return promise, low entry barriers, closer to end-consumers, focused high capex with predictable cash flows and easy financial leverage under energy efficiency are some of important investment attractors.

The risks of operationalization of DF are still getting unearthed with less than 3-5 implementors. Most businesses are intuitively betting on capitalising the high ATC losses in range of 30-50% in DF selected areas. The 15-20 years DF contracted period with estimated 4-5 years to bring losses to range of 15% makes viable ROI.

While the credibility of delivery from new players is still to be tested, there stands a strong chance of these new players bringing professionalism, technology, IT, measurements driven performance, analytics, strong SLAs (Service Level Agreements), and much forgotten customer focus back to the utility business.

Under light of this, is DF a good PPP model? Does it has potential to scale? We will continue sharing our views and also from best industrial experts on this in coming articles under label of ‘Smart Distribution’.