With ongoing operationalization of Distribution Franchisee (DF), one common question that keeps hitting again and again is ‘Why need of DF? What it can do, which utility cannot or have not?’. While answer to this is pretty subjective, I would share my opinion in 3 breakups

Key issues that are affecting profitability of distribution utility

What are key issues with Distribution Utilities?

How that has constrained key stakeholders potentials?

Does Distribution Franchisee has solutions to above?

Link from Measurements (MIS) to Effective Distribution Management missing

Lack of Incentivization

PSU Organizational Constraints

No Investment in skill enhancement

Low Enforcement

Govt. hindrance & manipulation

Low Accountancy

Key stakeholders revenue potential constrained with missing last-mile robustness

End consumers not getting reliable, sufficient and rightly priced power

Generators unable to get guaranteed evacuation of all generated power

Distributors (Utilities) themselves in losses

Power Traders do not have predictability

Does DF has a solution to above

At the end of day, it will do same thing as utility, but with a difference – more concentrated ownership that will expedite decisions to actions. Another way to look upon it will be as an extended ‘Business Outsourcing’ model, wherein the Franchisee becomes the new front end to the end-consumers, but assets still remains on book of the original Utility. The real underlying phenomenon driven by franchisee model is

Performance benchmarking through establishing baseline

Incentives alignment of all stakeholders

It is this ‘Measurements and Analytics’ that will drive the change and bring above suggested values to all stakeholders.

An obvious question with so much projected on Distribution Franchisee (DF) model is:

What real gains both the utility and end-consumers could expect coming out of the Distribution Franchisee model?

While Bhiwandi implementation of Distribution Franchisee has shown increased consumer satisfaction for improved service levels, but it is yet to be proved conclusively that the model has brought any significant monetary gains to the utility. The slow emergence of a potential impactful model (distribution franchisee) amidst opposition – from utility employees and end-consumers, could be attributed to missing INFORMATION and transparency. Opposition from utility employees is obvious as DF with its flavor of privatization is based upon driving cost efficiency by increasing productivity and hence reducing on numbers of utility employees. But opposition and fear from end-consumers is little less understood, when it doesn’t matter that same power at same tariff (decided by State regulators & common to the state) comes from utility or DF. May be this fear from end-consumers has some roots in weaken regulation/enforcement or mis-information or perceived apprehensions.

In any case, going forward there are many questions, that needs clarification to smoothen resistance, but more importantly to engage all stakeholders well to co-create sustainable solutions. A few of importance are:

With reduced AT&C losses from 50+% to order of 15% and reduced administrative & operations costs, could it be expected to see decreasing power tariffs (or atleast no changes for 5-10 years inspite of rise in power procurement costs) as realised by end-consumers? If and how does DF monetary gains could be shared with its end-consumers?

Since there is only one state level tariff plan prepared, consolidating audit reports from each circles/zones, the good and bad performances of different circles (including that of Franchisee’s) get mixed to create one tariff plan. So in such case unless more decentralization penetrates in distribution, that DF circle end-consumers cannot expect their tariff plan alone to be improved. If however DF model scales all through out the state, then combined benefits could still bring common savings to all state end-consumers.

Above would also mean that even if one circle’s management did a poor job of cutting its AT&C losses, there is no way of penalizing them independently. The entire state end-consumers get penalized equally. This is one serious missing incentive structure that has plagued utility’s performance.

How does exactly DF implementation improves profitability of the utility?

What are financial calculations that local utility has to consider to make a strong case for bringing in Distribution Franchisee over business-as-usual case? What profits (if any) can utility expect by leasing out its assets for 15 years to Distribution Franchisee?

How does the effective cost of distribution to local utility is accounted in setting benchmark input rates and its locking for next 15 years? We only hear the price realization terms like ABR (Average Billing Rate) and tariff setting term ARR (Aggregate Revenue Requirements) in RFP, but no comparison of these with actual cost of distribution.

Has post DF termination and appropriate depreciation of assets already being accounted in investment decision making?

Is utility prepared to take charge again post DF tenure or will it re-lease another DF term or there will be full privatization?

Total 1.1 lakhs Rural Franchisees in India (detailed distribution given below)

This covers only 19% of total villages in the country including both the RGGVY and non-RGGVY villages

Only 38% RGGVY villages are covered under Franchisees, when all are supposed to have mandatory Rural Franchisees

95% of total Rural Franchisees are Revenue Collection based Franchisees

Bihar, Gujarat (91%), Haryana (91%), Karnataka (73%), Nagaland, UP and West Bengal have above national average (i.e. 19%) Rural Franchisees in RGGVY villages

2. Rs. 26000 cr. already spent in last 6 years since 2005 and estimated another same amount to be spent (totaling to Rs. 52000 cr.) for coverage of RGGVY original targets of 100% village electrification and 2.34 cr. rural BPL household connections.

Since 2005, 96562 villages have been electrified raising the level of ‘village electrification ’ from 74% to 91%. (Total villages in India is ~6 lacs, out of which 1.25 lacs did not have access to electricity in 2005)

Since 2005, 1.75 crores rural households are given new connections raising the level of ‘rural household electrification’ from 43% to 56%. (Total # of rural households in India is ~14.5 crores, out of which 7.8 crores did not have access to electricity in 2005)

3. By estimate of investment, of order Rs. 52000 cr., RGGVY scheme is comparable to R-APDRP scheme of GoI.

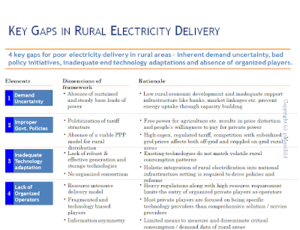

Rural ‘Power’ Inclusion: As Prayas’s paper identified there has been significant progress in grid extension and household connections through RGGVY, there remain broader questions to build answers for broader rural ‘power’ inclusion:

Quality of work and power supply

Sustainability of the infrastructure

Contribution to local (i.e. rural) development

‘Rural Franchisees’ is definitely one key to unlock rural power inclusion in India. There is strong need to innovate & integrate ‘Distribution/Delivery’ of power with:

Local ‘Distributed Generation’ of power

Strong policy initiatives to allow better grid interaction/sharing and localised tariff setting

Strong governance and independent monitoring of customer satisfaction

Market Opportunity comparison:

A simple comparison of the ‘existing’ market size (both in terms of numbers and contract values) of Distribution Franchisee opportunities between Rural and Urban, seems to point Rural as a winner. However challenges remains with some key gaps identified below in delivering rural electricity.

Question is what could be learnt from solving these ‘rural’ specific challenge with so much investment already gone into it and still more to come? What will be the applicability of those learning to broader Power Distribution markets? Could that lead to ‘disruptive innovation’ for improving financial health of utilities in India and improve Distribution efficiencies? Who amongst private players will bring that ‘market inflection’? Will the teachings of late Prof. C.K. Prahalad on ‘Fortune at the bottom of pyramid’ be applicable to this sector and who will set the first path?

One possible Strategy for entry into Distribution Franchisee:

There are already great efforts from many new players to enter into upcoming Distribution Franchisee bids (at district level like as in Madhya Pradesh) and they face tough competition against tough terms and conditions (like high ‘reserve rates’, strong qualification criterion, high EMD & security deposits etc.). It is possible that these new entrants or even established private companies also consider building first hand experience from participating in lower capital risk Rural Franchisees and bring their private corporate management best practices to establish reforms and innovations. With 1.1 lakhs rural franchisees and that covering only 19% of total villages and already invested Rs. 26000 crores, this could provide an easy and fastest entry to build most direct experience in the sector and participate in bigger bids more strongly, with more experience and hopefully at lowest rates with best workable technology.

Not to say that the Rural Franchisee experience would be easier than any urban franchisee or to be treated with less care. Infacts as highlighed above, the odds are higher in rural region and demands innovation. But the one who can cracks this rural challenge of power distribution will definitely emerge as a leader in this space with direct mapping of his skills set to urban challenge, but not the vice-versa for its otherwise competitors. Recent upsurge of ‘mobile’ market and ‘financial inclusion’ in rural are clear examples, that even in POWER sector, its time to offer more ‘choices’ to the end-customers and specially ‘Rural consumers’ be looked upon as profitable and respected segment (See earlier blog – Why Customer’s Satisfaction & Preferences are important for Electricity Utilities?).

At pManifold, we intend to undertake more detailed gap analysis with operating Rural Franchisees and help them Organize-Manage-ScaleUp. Interested stakeholders with willingness to support this cause and study, please contact Rahul Bagdia @ rahul.bagdia@pmanifold.com (+91 95610 94490)

pManifold as Knowledge Partner to IIES 2011 organized a workshop on ‘Solar PV System – Technology, Risks, Manufacturing, EPC, O&M, Investment’. The workshop brought best Industry experts and participants through out the country.

Role of components: Modules, Inverters, Racking, Trackers, Processes. How each of them play a crucial role in Levelised Cost of Energy (LCOE)

India specific challenges & Trends

PPAs & what are they good for

Solar Module Manufacturing

Different type of Solar Cells

How mono/multi crystalline modules is manufactured

Composition of modules

Machines required for manufacturing

Process of manufacturing

Testing of Solar Modules / Standards & Certifications

Important aspects in Module manufacturing

Investment and rough estimation on cost of project

Rough estimate on cost of manufacturing

Central & State Govt. Incentives – How to choose the right location

Financing Solar/RE – Bankers Perspective

What is the mindset of a Banker (from a risk point of view)

How should a Project Promoter think towards De-Risking a Project Proposal

Is there an ideal Equity/Debt mix that is better and more attractive from a Bankers perspective (will increase the financing chances)

What are the key decision makers / departments in SBI that will handle Renewable Project Finance

What is the typical timeline associated with a Project Finance Proposal (avg. time between receiving a proposal and release the first tranche of funds)

Off-Grid / Rooftop Solar Solutions for Buildings

Sourcing of components: please outline what are the best sources / companies for buying other (non-PV) components (Racking / Inverters / Cables / Junction Boxes / Monitoring)

Price trends for 2010-2011 — any geographical trends within India (North India vs. South, East, West)

Rupees per Watt – how does that change for a 1 KW system vs. 10 kw system vs. 100 KW system

Should one go for the lowest cost PV panel available in the market

Prevalent payment terms in the Industry (upfront / on delivery / on installation)

Consumer products – applications and potential

Examples of product

Current cost per unit installed

Approximate Breakdown of the cost

In what circumstances are they economical

Subsidies, if any

How easy is the installation process

Lifetime, Reliability and Servicing issues

Field Experiences – What Customers say

Speakers of the workshop

Akash – CEO, Indis Energy K.E. Raghunathan – MD, Solkar Solar Industries Ltd. Abhijit Chakravarti – AGM, State Bank of India Rahul Bagdia – Director, pManifold Business Solutions Adithya – R&D Head, Intelizon Energy Pvt. Ltd.

The workshop was organized under pManifold’s Stakeholder Engagement services. Focussed emerging models with potential to solve Indian power sector challenges were selected in categories of Distribution, Conservation and Generation. Relevant stakeholders including service providers, businesses, investors, bankers and professionals including students were brought together to participate in discussions led by domain experts to come with action items to scale respective business models. More details on each workshops on our Insights page.

The guidelines for second batch under Phase I of Jawaharlal Nehru National Solar Mission (JNNSM) were announced recently by Ministry of New and Renewable Eneergy (MNRE) . The excerpts of the guidelines are captured in our previous blog.

To give strong impetus in promoting domestic manufacturing, the developers are expected to procure their project components from domestic manufacturers. For Solar Photo-voltaic (PV) projects using Crystalline technology, to be selected in second batch during FY 2011-12, it is mandatory for all the projects to use cells and modules manufactured in India. However, Thin film and Concentrated PV (CPV) has no such domestic limitations.

In view of the above, the list of major Indian players in Solar Cell and Module manufacturing along with Technologies are mentioned below:-

The above list may not be a complete and comprehensive list, but it gives an overall and fair representation of players involved in manufacturing of solar cells and modules.

What is to be seen if the domestic content constraint on Crystalline technology and its relative higher costs compared to Thin film will force new projects to go with Thin film technology

Also there will be competition amongst Crystalline panel manufacturing players to get share of batch-2 projects and this could drive new market dynamics

pManifold as part of its Solar practice offer services to properly reveal and pen down the technology, cost and performance trade-offs. (See pManifold services in Solar for more details)

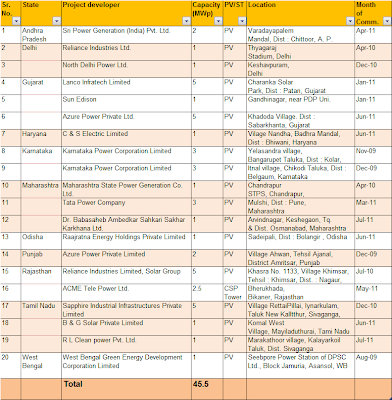

MNRE has recently released the list of all grid operating solar PV projects in India (latest updated as on July 2011. See the detailed list here and also below).

The Project Developers for these cumulative 45.5MW capacity plants were:

Sri Power Generation (India) Pvt. Ltd.

Reliance Industries Ltd.

North Delhi Power Ltd.

Lanco Infratech Limited

Sun Edison

Azure Power Private Ltd.

C & S Electric Limited

Karnataka Power Corporation Limited

Karnataka Power Corporation Limited

Maharashtra State Power Generation Co. Ltd.

Tata Power Company

Dr. Babasaheb Ambedkar Sahkari Sakhar Karkhana Ltd.

% Capacity Utilization Factor- CUF (Average over period of operation, Maximum, Minimum)

Some key observations made:

Avg CUF or Plant Load Factor (PLF) across the year is in range of 15-19%

Peak CUF occurs in March to May and range from 20.21% to 23.63%

Grid synchronization takes 2-4 months initial settling period with CUF going down to less than 10%

The report is first good step in monitoring performance and stakeholder engagement. However a big leap in monitoring solar plants performance and integrating the analytics to design appropriate solutions has to still happen.

A comparative view of top level findings is shown here, developed using the location specific reports of Shajapur, Ujjain & Dewas available here along with 6 other districts in Madhya Pradesh (MP).

The analysis shows that in the above 3 districts, a substantial percentage of dissatisfaction in

Customers is coming due to 2 factors, namely ‘Communication’ & ‘Price’.

The overall Satisfaction score on being computed(on scale of 0-100 with 100 being all respondents ‘very satisfied’):

Communication

Price

Shajapur

33.68

30.76

Ujjain

27.09

32.77

Dewas

24.50

20.90

The main reasons for higher dissatisfaction across the 3 districts as indicated by the customers are due to following:

Less ‘Awareness’ from Utility regarding the attributes ‘Energy Efficiency’ & ‘Consumer Rights’

Less communication for ‘Advance notice about disruption’

‘Power Tariff & its variations’ is High

‘Shajapur’ district has higher percentage of customers agreeing towards ‘Privatization’ of Power Distribution compared to ‘Ujjain’ & ‘Dewas’

On being asked if “Service levels will improve

if a private company manages electricity

distribution”, the responses of different

districts were as follows:

Shajapur – 44%

Ujjain – 39%

Dewas – 31%

Across different categories of consumers, over 50% respondents from ‘Commercial’ customers in ‘Dewas’ and ‘Shajapur’ districts agree that ‘service levels will improve if a private company manages

power distribution’.

Approximately 20% respondents from all the 3 districts ‘Neither Agree nor Disagree’ with ‘Privatization of Power Distribution. Also, ‘Agri’ customers have considerably lower expectations (<40%) in ‘Dewas’ & ‘Ujjain’ districts with ‘Privatization’.

This is the summary of results from the top level analysis, developed using the ‘Consolidated Report’ of all the 9 districts in Madhya Pradesh (MP).

Across all 9 districts, expectations of customers based on certain factors like Customer Service, Power Quality & Reliability and Price are significantly leading to high Dissatisfaction among all categories of customers i.e. Residential, Commercial, Industrial & Agri. Following attributes of above factors need prior attention as suggested by customers:

Unplanned / Planned Outages

Local Electricity Infrastructure

Resolution Billing Complaints

Resolution Meter Complaints

Service Response Time

Value for money

Fairness of Price

Customers Agreement Levels of ‘Distribution Privatization’ through franchisee model in all the 9 districts

83% respondents from ‘Bhind’ district agree with positive impact of ‘Distribution Privatization’ followed by 51% respondents from ‘Gwalior’.

Only 28% respondents from ‘Sagar’ district agree with positive impact of ‘Distribution Privatization’, which is the lowest of all the districts.

Customers have high expectations from utility to improve the current system & make them fully satisfied

Over 55% respondents from all the 9 districts agree that lot needs to be done to improve the current utility system and make them fully satisfied with ‘Bhind’ district has expectation with 91% & ‘Datia’ district has lowest expectation with 56%.

The Ministry of Power Govt. of India issued a directives for implementation in the all States of India, after seeking consultation with Ministry of Law and Justice and said that,

“Section 42(ii) read with the first and fifth proviso is a self-contained code with regard to consumers who required the supply of electricity of 1 MW and above and accordingly the State Electricity Regulatory Commissions cannot continue to regulate the tariff for supply of electricity to any consumer of 1 MW and above”.

“The provisions of section 42 need to be analyzed in relation to the duties of the distribution licensees and open access. While sub-section (2) requires the State Commission to introduce open access within one year of the appointed date the fifth proviso makes it mandatory for the State Commission to provide open access to all consumers who require supply of electricity where the maximum power to be made available at any time exceeds 1 MW. The fifth proviso was introduced by Act 57 of 2003 with effect from 27th January 2004”.

“The first issue is if open access is made obligatory whether the distribution licensees will continue to have the responsibility of universal service obligations with regard to consumers whose requirements are in excess of 1 MW. An analysis of the various provisions (particularly section 49 of the Act) shows that if certain consumers want to have the benefit of the option to buy power from competing sources, then it is logical that DISCOMS do not have an obligation to compulsorily supply power to such consumers. If such consumers want power from the DISCOM then the terms and conditions of the supply would be determined in terms of section 49 of DISCOM also”.

“There is no conflict between the aforesaid conclusion and the provisions of section 42(3) of the Act which provides that a person requiring supply of electricity has to give notice in respect thereof. If the consumer intends to use the network of the DISCOMS, he has to give notice and upon such notice to DISCOM (it) is duty bound to provide non-discriminatory open access to its network. Section 42(3) cannot be construed to mean that giving of a notice is a pre-condition for the implementation of open access”.

The directives issued by MoP shall have great impact on power sector particularly Electricity consumers, generators, traders and power market. There are positive as well as negative sides which are to be looked into minutely. The Commission will have a great responsibility to implement the suggestions of MoP by making suitable Regulation as well as to protect consumers against some negative points which are elaborated below.

POSITIVE POINTS

Consumers of 1 MW and above are deemed OA consumers and shall have choice of purchase of power from cheaper sources including Discom.

The tariff of such consumers shall not be regulated by Commission and the heavy burden of cross subsidies shall not be loaded to such consumers.

Such open access consumers shall not be required to pay cross subsidy surcharge because the tariff of such consumer shall not be decided by the Commission, such consumer shall not be consumers of Discom, the power requirement of such consumers shall not be a part of ARR of Discom.

According to National Tariff Policy the cross subsidy surcharge is linked with tariff for the category of consumer, decided by the Commission who are going out of net of Discom because of open access hence Discom is to be compensated by cross subsidy surcharge but there shall be no such requirement in the changed scenario hence such consumers will not have to pay CSS on the power wheeled through open access.

Discom / Transmission Licensee shall be benefited by collecting wheeling & transmission charges as an additional income over and above the income from retail sale of power to the consumers below 1 MW.

Power purchase quantum of Discom shall reduce and shall be limited only equivalent to supplying power to the consumers below 1 MW and Commission shall decide the tariff only for consumers below 1 MW hence ARR of Discom shall be substantially reduced.

Sufficient power shall be available to Discom from Genco plants at cheaper rate to supply power to consumers below 1 MW and total load shedding shall be withdrawn to such consumers. Expenditure account of Discoms shall reduce because of reduced employees strength and reduced working capital requirements hence tariff for consumers below 1 MW shall reduce.

Power generators and traders, who are unable to supply power due to denial of open access and being put to financial loss, will have increased demand for power to supply to consumers of above 1 MW and shall be benefited due to increased in rates of power.

Demand of power from power exchanges shall increase.

NEGATIVE POINTS

All the Consumers above 1 MW will have to find their own supplier for power.

Rates of power in market shall increase due to increased demand.

Power source to supply power to all consumers above 1 MW in the state may be limited since the large producers of power have already entered in to PPA with different bulk purchasers. Hence the small consumers may not get power to their requirements from open market or power producers and will have to approach MSEDCL who may refuse to supply power due to non availability or may charged exorbitant rates since the tariff shall not be regulated.

All consumers above 1 MW will have to install ABT meters which will be an additional expenditure. Further till now the specifications of ABT meter has not been framed. The Discom & Transco have different specifications of ABT meter and open access consumers are suffering due to this discrimination in the specifications.

Availability of ABT meters is limited hence cost of meters shall shoot-up due to heavy demand. There is only one supplier approved by Transco who is taking undue advantage of monopoly.

The consumers opting power from power market shall have to find another source also who can supply infirm power and such power can be supplied only by Discoms who may charge high price of power since it is not Regulated by Commission.

SLDC and NLDC are not equipped to handle such large O.A. consumers.

SUGGESTIONS FOR PROTECTING CONSUMERS FROM ABOVE REFERRED ODDS

Commission should frame Regulations for implementing the directives after due public opinion which should include following:

The provision of O.A. for all consumers above 1 MW is to be introduced in phased manner as below:

1st phase – All EHV consumers and all the consumers above 5 MW of power including all consumers above 1 MW who want to opt O.A

2nd phase – All consumers above 3 MW of power.

3rd phase – All consumers of 1 MW and above.

Decide infirm power tariff / stand by demand for O.A. consumers who opt the same from Discom.

Separate retail sale and wire business of Discom and Transco.

Make amendments in pending Draft O.A. Regulation and call fresh comments from consumers and stake holders.

Decide common specifications of ABT meters for Discom & Transco.

Make provisions to strengthen SLDC and issue guidelines for working of SLDC.

Invited post from Mr. R.B.Goenka (Mr. R.B.Goenka is Consumer Representative @ MSEDCL and associated with Vidarbha Industries Association)

Disclaimer: Above are independent opinion of external expert and should not be associated with pManifold or any of its team members. pManifold deem this new Open Access directive very important and will continue bringing different stakeholder’s perspectives. The issue deals with consumer choices, electricity infra sharing & management, tariff calculations, power trading, industrial economics etc.

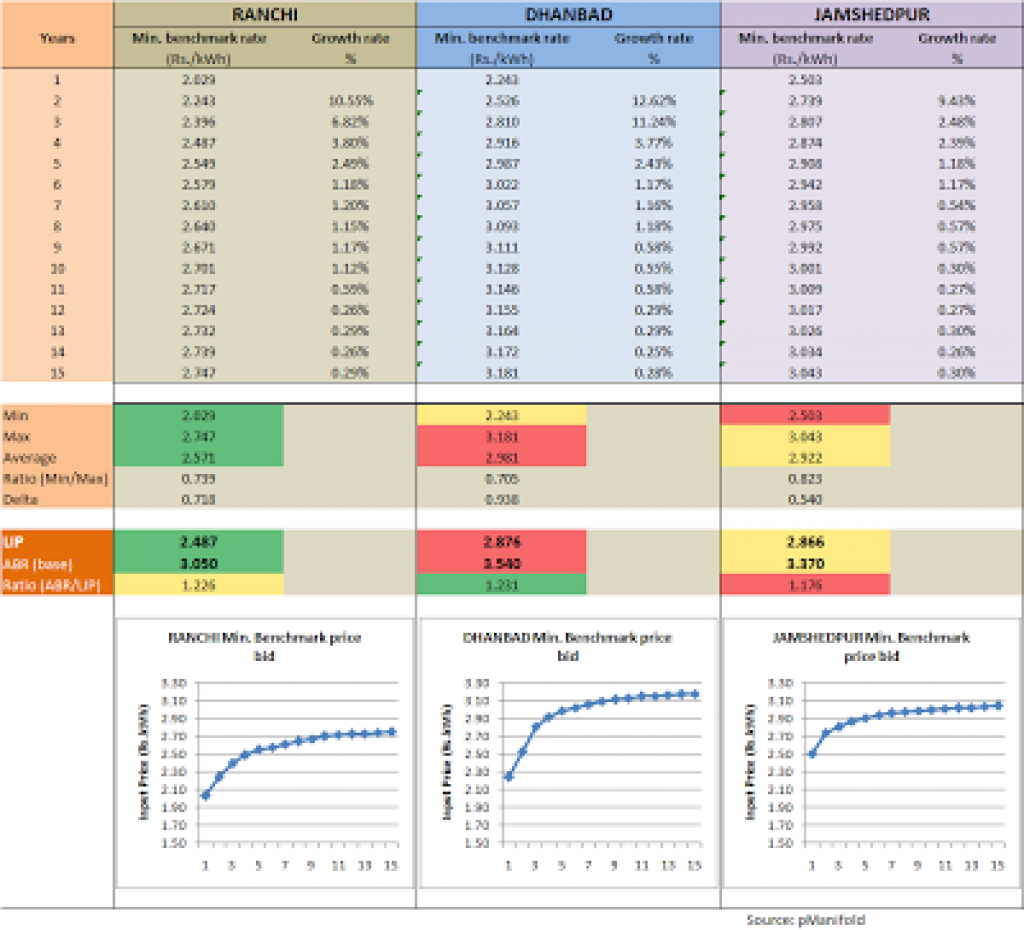

JSEB has given minimum benchmark input price curve for all the regions, mandating bidders to bid higher than given price curve for all 15 years. The bidders in pre-bid meeting has earlier requested to have no benchmarks, to allow them innovating on financial structuring. (See our blog Jharkhand Distribution Franchisee first pre-bid meeting)

See below table with useful bid analytics

Some top level observations:

Steep growth rate of around 10% in initial first 2 years, with max. in first year; followed by receding growth rate to 2% by 5 years; almost stable and slow receding of around 1% until 10 years, and then another stagnant increase of less than 0.5% and below until 15 years.

Ranchi has lowest start point around Rs. 2/kWh, with Jamshedpur highest at Rs. 2.5/kWh

Ranchi again has lowest end point around Rs. 2.75/kWh, with Dhanbad highest at around Rs. 3.2/kWh. Amongst 3 DF regions, Dhanbad ranks lowest in geographical area, highest in consumer density and highest in AT&C losses. This probably be the reason for its highest end point pricing, because otherwise it ranks lowest in most other metrics of pManifold’s DF attractiveness matrix.

The ratio of max. to min. rates for each curve is higher than 0.7.

The highest ratio is for Jamshedpur, resulting into lowest delta of Rs. 0.540 between the max and min rates of price curve.

The lowest ratio is for Dhanbad, resulting into highest delta of Rs. 0.938 between the max and min rates of price

The Levelised Input Price (LIP) calculated at discount rate of 11% is highest for Dhanbad at Rs. 2.876/kWh, followed by Jamshedpur, with lowest for Ranchi at Rs. 2.487/kWh. (Difference of around 40 paise).

Average Billing Rate (ABR) of Ranchi is lowest at Rs. 3.050/kWh, revealing greater improvement opportunity for that DF. Dhanbad has highest ABR of Rs. 3.540/kWh, which is sort of contrasting with its highest AT&C losses, lowest revenue billing & collections, and also lower collection efficiencies (see Jhanrkhand’s DF attractiveness Matrix for details)

Ratio of ABR to LIP is highest 1.231 for Dhanbad, 1.226 for Ranchi and lowest 1.176 for Jamshedpur. (This ratio is static indication of profit margin for bidders, with close to 1.00 value is indication of lower margins and higher risks for DF operator)

pManifold’s DF bid advisory services further augment our client’s bidding strategy through consolidation of on-site (network and customer) intelligence and other secondary research on electricity value chain for the region and its customer’s demographics (socio, economic, political, cultural). Also our Discom Advisory services provides support in preparation of baseline data for new coming DF regions, and integrated financial modeling of Distribution Licensee and Distribution Franchisee to study various trade-offs to design robust DF model and contract for true win-win of Discom and DF.