Lithium-Ion Batteries (LIBs) take up ~40-50% cost of EVs, with its approx. one-third cost in materials, one-third in battery pack and last one-third in BMS. India is projected to have ~200 million EVs by 2030 on road, with then estimated cumulative ~1000 GWh LIBs in the system, and continuing annual addition of ~150-200 GWh in following years.

The value chain of LIBs shall constitute material supplies, cell manufacturing, cell to battery pack manufacturing, and BMS manufacturing. Further it shall be OEMs who shall integrate the LIBs in their vehicle, with main interaction with i) EV Charging circuit

ii) Discharging circuit (including Power Train drive)

iii) vehicle electronics & communications

iv) battery and/or vehicle cooling. The end-users care for (long) range, (faster) charging time, (higher) top speed and acceleration and lower TCO from their EVs, and these attributes has high interrelation with choice of battery, its management and cost trade-offs.

Battery pack design, thermal management, BMS and Vehicle Integration – all four plays very important role to get best value of the costliest single component in EVs.

This Webinar topic was focused on:

Understanding Battery Pack and BMS key constituent elements and their design rationale for new age EVs in India

Learning different practices for Battery Thermal Management and arising challenges and advantges

Learning from different testing results on key fail safe criterion for LIBs to build effective battery control and management for optimal battery-vehicle performance and high battery life

What competencies and edge India can focus to grab sizeable market share in battery manufacturing and BMS

India has some 52 STUs/SPVs operating with some 1.47 lacs bus stock (till FY 2015-16). Out of this total stock, rural share is 80%, urban is some 17% and hilly region is 3%. In the same year, ~7,250 new buses were annually added with 85% market share between only two companies.

In the same year, similar ~6,500 number of buses were scrapped. Total revenues in FY 2015-16 were INR 51.75K crores with INR 12.63K crore losses. Only 7 of total 47 reporting STUs showcased profits (Karnataka SRTC, BMTC, UP SRTC, Punjab Buses, Odisha SRTC, Kadamba TC (Goa), and Himachal (HRTC).

e-Buses with current technology roadmap holds potential to provide cleaner public transport advantage at comparable Total Cost of Ownership (TCO) with existing diesel options. pManifold analysis shows that current diesel bus operation costs some 58 Rs./km, while that of e-Bus with 100km range can cost comparable 57 Rs./km.

Increasing range to 200 kms can cost some 61 Rs./km. GOI in one of its tender has supported procurement of 390 e-Buses under FAME scheme for 11 cities. The bidding results are out, but there is still e-Buses to be seen operational under this tender, though small pilots with some STUs are in progress.

While cleaner air will be one important outcome from e-Buses adoption, it will be important to understand if and how they also emerge as techno-commercial viable option for STUs, and what more and right needs to be done today.

This webinar focused on:

Understanding business proposition for e-Buses to STUs

What problems of STUs e-Buses can solve, and what it cannot

What business models for STUs to finance and operate e-Buses including charging and maintenance

What considerations for STUs to procure e-Buses, and for cities to integrate e-Buses appropriately

Speakers

H. K. GuptaChief General ManagerHimachal Road Transport Corporation (HRTC)

Laghu ParasharSenior AdvisorUrban Mass Transit Company Limited (UMTC)

Rahul BagdiaDirector and Co-founderpManifold Business Solutions Pvt. Ltd.

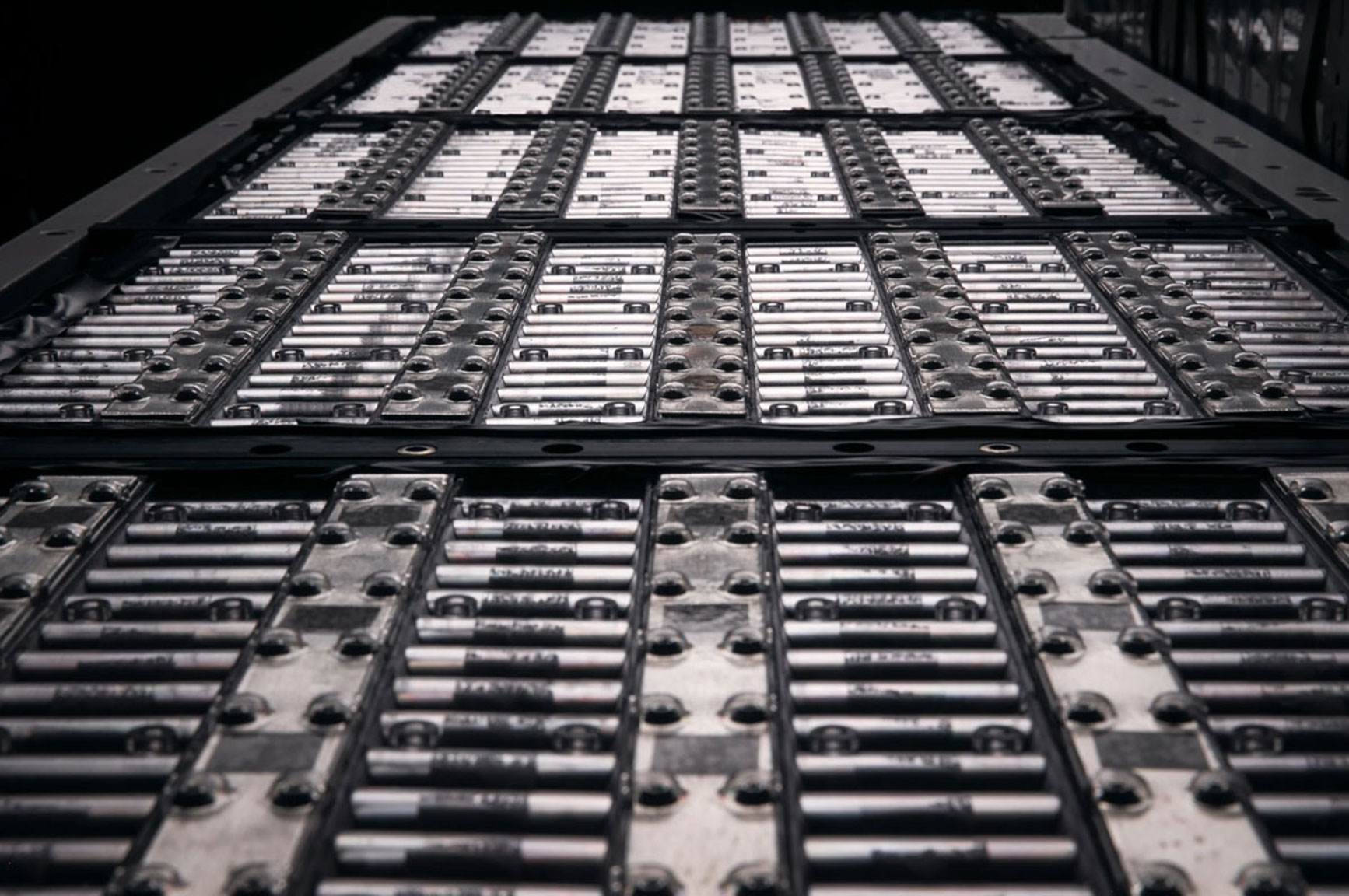

LIB Reuse and Recycling – Creating Secondary Market for Batteries in India?

Today 40-60% of EV cost comes from LIBs. If there can be a fluid secondary market for scrap batteries (derived from second life use and recycling), then there will be certainty in resell value for LIBs, which will then allow building the right financial loan instruments for EV financing. Additionally, LIB recycling ensures adding to the supply of otherwise scarce precious metals back into the system.

LIB recycling is an emerging new industry globally. ~50% of spent LIBs assets are recovered and recycled in Europe, China, South Korea, and Japan. In contrast, less than 5% of all LIB assets are recycled in the US. While cobalt and lithium are thought to be the two most valuable metals found in Li-ion batteries (with consumption of both reportedly outpacing production in the last couple years), other metals like iron, nickel, aluminum, and magnesium also have positive revenue implications when recycled.

India stands at the early stage of seeing EV and Energy Storage influx, which in later years will constitute the highest share in overall LIB waste. If it can regularize LIB waste through strengthening reuse and recycling eco-system, it will go a long way in securing its EV supply chain, and also driving adoption with improved EV financing.

In this webinar, we shall focus on:

Why India should worry about reuse and recycling of LIBs?

How to ensure 100% LIBs from EVs come for recycling?

What technology options for efficient and viable LIB reuse and recycling?

What policy measures to improve LIB recycling in India?

Understanding EV customers: What is required to increase EV adoption in Indian cities?

India downsize its 100% new sales target for Electric Vehicles (EVs) to 30% by year 2030. Achieving this revised target will not be easy journey, and specially so with big democracy and diverse country it is. The diversity at city level is huge, and this provides both challenges and opportunities. It was industry participation and city level entrepreneurship traction that resulted into early pilots in e-Mobility in India, despite Centre delays in announcement of dedicated National e-Mobility Mission.

Government has important role in setting targets, streamlining actions between different stakeholders and guiding early investments. But ultimately, it will be market forces that has to sustain e-Mobility development and its right scale-up.

A big question comes as how these market forces can be developed speedily and coordinated for more and more well integrated EVs deployment in cities. The EV team at pManifold has pilot studied 10 Indian cities through mix of primary and secondary research and built insights on performance, expectations, challenges and preferences by actual EV users (across 2W, 3W and 4W), potential EV buyers, EV dealers and charging operators.

The insights developed can help EV community including cities to bottom-up strengthen their EV planning and deployment in areas of

1) Product Development

2) Production Supply Chain Strengthening

3) Charging Infrastructure and Services

4) Financing

5) Institutional structure for policies execution across different departments.

In this webinar, we focused on:

Key insights from stakeholders for city level EV adoption

City EV Readiness Scorecard developed by pManifold

Comparative city EV readiness (for piloted 10 cities)

India is aiming to lead EV race with the latest push in the budget. The government have set a target to reach a 30% sales share for EVs by 2030. To practically achieve this target, the market will need a commitment of EV-friendly policies, consumer awareness, vehicle charging networks, and manufacturing capabilities.

In automobile industry, dealers play a significant role in market penetration, they are the customer touch point responsible for sale and post-sales service support. EV being new technology, the customer awareness or acceptance is low, resulting into low sales volumes. As a result, many EV dealers are struggling to increase their sales. Therefore, it is important for all stakeholders to understand the dealer’s outlook in EV as they provide ground-level facts and help to understand the product feedback, EV demand-supply scenario, and possible pathways to increase the EV sales.

This webinar has addressed below concerns of EV Dealers:

How economical is to own e-2W and e-3W when compared to ICE based vehicles?

What marketing activities are leading to better sales? What support from OEMs could further drive EV sales?

Is EV dealership a good opportunity?

What are the learning, experiences and customer feedback around EVs? (with some case studies)