With the projected demand for Li-ion batteries set to reach 235 gigawatt hours (GWh) by 2030, recycling has become a focal point. This emphasis aims to ensure a sustainable supply of raw materials for cells and decrease reliance on imported resources. Extracting materials through recycling Li-ion batteries is more sustainable than mining. Moreover, the limited availability of key battery materials like lithium, nickel, and cobalt further strengthens the case for recycling.

It was found that recycling has the potential to reduce primary demand compared to total demand in 2040, by approximately 25% for lithium, 35% for cobalt and nickel, and 55% for copper, based on projected demand. This creates an opportunity to significantly reduce the demand for new mining.[1]

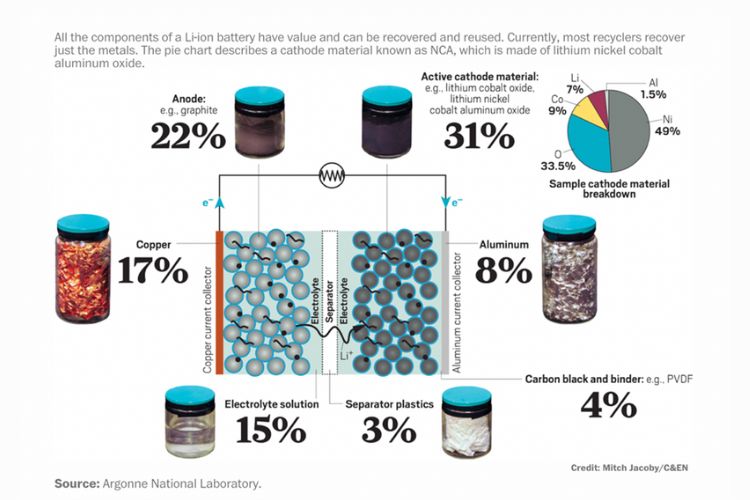

Lithium Ion Batteries (LIBs) have multiple components that contain valuable metals and non-metallic materials that can be recovered during recycling. The materials recovered could be used to make new batteries, lowering manufacturing costs. Currently, those materials account for more than half of a battery’s cost. In many cases, batteries—especially in vehicles—are retired from their first use but can be repurposed for secondary use, such as stationary storage. The prices of two common cathode metals, cobalt, and nickel, the most expensive components, have fluctuated substantially in recent years.

Market size: Global vs India

The global battery recycling market is valued at USD 26.9 billion in 2023 and is projected to reach USD 54.3 billion by 2030, growing at 10% CAGR during the forecast period.[2]

The figure above illustrates the cumulative demand projections from 2022-30 for lithium-ion batteries in India and the corresponding recycling volumes.

It is estimated that the cumulative potential of lithium-ion batteries in India from 2022-30 across all segments will be around 600 GWh (base case) and the recycling volume coming from the deployment of these batteries will be 128 GWh by 2030. Out of which almost 59 GWh will be from the electric vehicles segment alone.

Components of a Lithium-ion battery that can be recycled

Ion cells: These are the primary energy storage components of the battery. Recycling involves extracting materials like lithium, cobalt, nickel, and other metals from these cells. During the Preparation stage of recycling, the battery management system (BMS) containing the Li-ion cells is separated from the battery. Through further dismantling stages and treatments, various materials are recovered from the cells.

Cathode: Typically, the cathode contains materials like lithium cobalt oxide (LiCoO2), lithium manganese oxide (LiMn2O4), lithium iron phosphate (LiFePO4), or other metal oxides. It undergoes various steps during recycling including Washing, Filtering, Pressing and Drying. Consequently, the materials of the cathode can be utilised as active material for new cells.

Anode: Often made of graphite or other carbon-based materials. Recovering graphite and other materials from the anode is part of the recycling process. Anode scrap that comprises critical materials such as graphite and valuable Cu can be recycled and reintegrated into the battery supply chain. Recovering graphite from anode scraps can provide battery-grade graphite without energy-intensive purification processes and can help support a domestic supply chain. Like the cathode, the anode also undergoes similar steps (Washing, Filtering, Pressing and Drying) during recycling which allow the graphite to be recovered.

Electrolyte: Generally, the electrolyte is volatile and cannot be recycled. However, in certain frontier technologies for recycling such as Hydrometallurgy, electrolytes can be recycled as well. Recycling electrolytes requires the use of activated carbons which absorb the electrolyte vapours. There may also be the need for an inert gas environment due to the volatile nature of electrolytes.

Separator: A porous membrane that separates the cathode and anode, typically made of materials like polyethene or polypropylene. Removal of the separator is carried out during the Pre-treatment phase of recycling when the cells of the LIBs are Disassembled. The separator can then be recycled and reused.

Metal Foils: Thin foils of copper and aluminium are used as current collectors in the anode and cathode, respectively. They are separated from the anode and cathode during the process of Washing. These foils can then be recycled and the extracted Copper and Aluminium are used in the electrical industry.

Plastic and Metal casings: The outer casing of the battery is often made of plastic and/or metal. Both materials can be recycled. The casing is removed during the Preparation phase of the recycling process itself when the battery is discharged and dismantled.

Bus Bars and Terminals: These conductive components are used to connect the battery to electronic devices. They are often made of metals like copper or aluminium, which can be recycled. Like plastic and metal casings, the bus bars and terminals are separated during the Discharging and Dismantling (Preparation) phases of recycling.

The following chart shows the summary of materials that can be recovered through different recycling processes.

Use Cases of Recycled Battery

Usage in grid-connected solar panels: batteries that undergo damage during transportation and manufacturing cannot be used for their primary purpose i.e., EVs. However, they can be refurbished and recycled to yield battery packs to be used alongside solar panels

Usage in power banks: Laptop batteries can be repurposed and used for power bank applications.

Other industrially valuable materials :

Copper and aluminum extracted from batteries’ busbars find use in the electrical components industry

Nickel, Cobalt & Manganese are industrially valuable metals finding uses in the electrical, automotive, and housing industries.

Plastic extracted from the casings of the batteries also finds various industrial applications

India, as an agrarian nation, is witnessing a transformative shift in its agricultural landscape with the integration of renewable energy and productive use appliances. In the pursuit of sustainable practices, the adoption of clean energy solutions plays a pivotal role in enhancing agricultural productivity, reducing dependency on traditional power sources, and mitigating environmental impact. In this blog let us explore the significant impact of renewables and productive use appliances on sustainable agriculture in India, supported by compelling statistics.

India’s commitment to renewable energy is evident in its ambitious targets and policies. According to recent statistics, India is among the top countries globally in terms of renewable energy capacity. As of October 2023, the country has 178.98 GW of installed renewable energy capacity, comprising solar, wind, and other sources. This shift towards clean energy aligns with the goal of ensuring energy security and minimizing the carbon footprint associated with traditional agricultural practices.

The integration of productive use appliances, powered by renewable energy, brings about a paradigm shift in agriculture. The key PURE appliances including solar pumps and solar cold storage units are becoming instrumental in enhancing productivity, reducing post-harvest losses, and improving overall efficiency in the agricultural value chain.

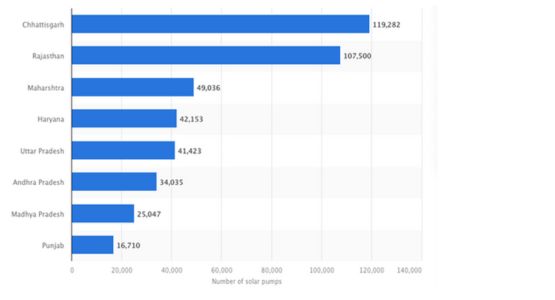

Solar Water Pumps: Harnessing abundant sunlight, solar water pumps offer a cost-effective and eco-friendly alternative to traditional energy sources. As per recent statistics 5.5. million SWPs are installed in India, benefiting thousands of farmers and enhancing agricultural productivity. This transformative shift not only reduces dependence on conventional energy but also positively impacts the livelihoods of farmers, particularly in remote areas with limited access to power infrastructure.

Figure 1. SWPs installed by State in India (Source: Statista)

Solar Cold Storage: As per FAO, almost 40% of the fresh fruits and vegetables worth 8.3 billion are lost as post-harvest losses, a longstanding challenge in Indian agriculture. The implementation of solar-powered cold storage units emerges as a promising solution as it not only ensures better income for farmers but also contributes to food security on a larger scale. However, certain challenges like high cost and market linkages need to be addressed to achieve their full potential.

“We urgently need to accelerate the build-up of solar energy, especially in developing countries and in applications that influence the daily lives of those without access to reliable energy – such as getting electricity from solar mini-grids, powering agricultural pumps, and running cold storages.” – Director General of International Solar Alliance, Dr. Ajay Mathur at the 6th Session of ISA at New Delhi

The statistics presented underscore the transformative potential of renewables and productive use appliances in Indian agriculture. As the nation strives for sustainable development, the continued adoption of clean energy solutions holds the key to ensuring food security, increasing farmers’ income, and mitigating the environmental impact of traditional farming practices. The power of renewables is not just in generating electricity; it’s in cultivating a greener, more sustainable future for India’s agriculture.

Clean cooking, despite its significance, is often overlooked as a policy priority. It must take centre stage on the global energy-climate-development agenda for reasons that go beyond convenience or preference. One third of the global population which is approximately 2.4 billion people worldwide remain without access to clean cooking. In India, nearly 60 percent of the population use traditional cookstoves. The issue of clean cooking is one of mammoth proportions.Unfortunately, millions of people continue to die prematurely each year from household air pollution, which is produced by cooking with inefficient stoves and devices paired with wood, coal, cow dung, crop waste or kerosene.

Clean cooking is an urgent matter of life, health, and environmental preservation. The harsh reality is that traditional cooking methods, relying heavily on fossil fuels and biomass, perpetuate a silent crisis that affects millions, especially women and children, around the world.

At the centre of this narrative lies the undeniable truth of its impact that it has on human lives. Every day, millions of households, primarily in developing nations, endure the burden of archaic cooking practices, where smoky open fires and rudimentary stoves fill their homes with toxic fumes. The World Health Organization estimates that nearly four million people die prematurely due to illnesses caused by indoor air pollution, with women and children being the most vulnerable victims. It is an alarming echo of injustice, a reality that demands immediate attention and substantial solutions. That’s more than the death toll from malaria, tuberculosis, and HIV/AIDS combined. The smoke generated by open fireseeps deep into the lungs, causing respiratory illnesses, lung diseases, and even cancer. It is a scourge that traps communities in a cycle of poverty, perpetuating inequality, and stifling development.

Moreover, traditional cooking methods are driving environmental devastation, amplifying the global climate crisis. As households burn wood and charcoal for cooking, deforestation accelerates, resulting in a loss of vital carbon sinks and increased carbon emissions. This deforestation contributes to climate change, contributing to rising temperatures, erratic weather patterns, and more frequent natural disasters. In developed countries, almost all households have access to clean cooking – electrical or LPG run gas stoves. However, in many developing countries, people cook on open fires and with inefficient stoves that run on wood, dung, or other polluting solid fuels. In numerous communities, women bear the greatest burden of household duties, including the adverse social and health consequences of lacking access to clean cooking. The lack of clean cooking is also an issue in remote communities that are not well connected to the national energy grid in middle-income countries.

However, hope shines through amidst the darkness. The adoption of clean cooking technologies offers a ray of light that can transform lives, safeguard health, and protect the environment. Clean cooking is a way of cooking which uses sustainable fuels and modern cooking technologies that allows people to cook and heat their homes in a way that does not harm their health and controls the immediate effects on their environment. By replacing polluting fuels with cleaner alternatives such as LPG, electric stoves, or solar-powered cookers, it is possible to reduce indoor air pollution and save millions from the clutches of respiratory diseases. Clean cooking is not just a luxury; it is a basic human right that can empower the women by freeing up their time that can be efficiently utilised for education, revenue-generating activities, rest, or leisure.Enabling them to escape the shackles of energy poverty.

Moreover, embracing clean cooking solutions is a key steppingstone towards achieving the United Nations Sustainable Development Goals. It is a pathway to empowerment, offering opportunities for women to participate in education, entrepreneurship, and the workforce. As women become agents of change, the ripple effects will resonate through entire communities, fostering inclusive growth and social progress. However, taking clean cooking to the forefront of our global priorities requires collaborative efforts from governments, industries, and civil society. We must invest in research and innovation to make clean cooking technologies affordable and accessible for all, regardless of their economic status. Governments should offer incentives and create supportive policies that spur the adoption of clean cooking solutions. And we, as consumers, need to make conscious choices that support sustainability and human well-being.

Clean cooking is not just a matter of convenience; it is a moral imperative. As we strive for a sustainable and equitable future, let us place clean cooking at the heart of our energy, climate, and development agendas. By doing so, we can create a symphony of change that resonates with hope, health, and harmony, for generations to come.

Global mean temperatures are projected to increase by 3.7 to 4.8°C, which would lead to catastrophic and irreversible effects on humanity and Earth’s ecosystems. In December 2015, the first global agreement of its kind was made when governments committed to maintaining the global temperature within this 2°C limit, to keep the temperature rise to 1.5°C – the Paris Agreement. It is a legally binding international treaty that sets long-term goals to guide all nations:

Substantially reduce global GHG emissions to limit the global temperature increase in this century to 2 degrees Celsius along with efforts to limit the increase even further to 1.5 degrees.

Review countries’ commitments every five years

Provide financing to developing countries to mitigate climate change

Industrial emissions are a major contributor to the global emissions landscape. A substantial portion of our electricity continues to be generated through the burning of coal, oil, or gas. These practices release potent greenhouse gases into the atmosphere, creating a heat-trapping blanket that contributes to global warming. Sectors such as manufacturing, food processing, mining, and construction further amplify emissions through various processes, including on-site combustion of fossil fuels for heat and power, non-energy use of fossil fuels, and chemical procedures involved in iron, steel, and cement production.

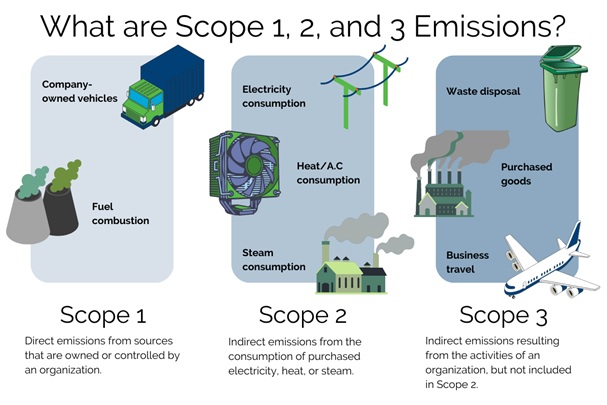

Businesses must reduce their environmental impact. One of the most significant ways to do this is by reducing their carbon footprint, and this starts with monitoring carbon emissions. But what are emission scopes 1, 2 & 3 (as defined by the GHG Protocol)

Often, emissions along the value chain represent the biggest GHG impact. For decades, companies have missed significant opportunities for improvement.

What is Net Zero?

Net zero means becoming carbon neutral. In simple words, net zero means cutting greenhouse gas emissions to as close to zero as possible, with any remaining emissions re-absorbed from the atmosphere, by oceans and forests for instance.

Governments have the biggest responsibility in the transition to net-zero emissions by mid-century. But businesses, investors, cities, states, and regions also need to live up to their net-zero promises.

Scope 1, 2 and 3 emissions

The term first appeared in the Green House Gas Protocol of 2001; Scopes are the basis for mandatory GHG reporting. Scopes provide a framework for categorizing and reporting GHG emissions, helping organizations assess and disclose their environmental impact. The emissions are broadly classified into 3 categories.

Scope 1 emissions— The Green House Gas (GHG) emissions that a company makes directly.

Scope 2 emissions — These are the indirect emissions that a company makes. For example – when the electricity or energy it buys for heating and cooling buildings, is being produced on its behalf. An organisation can source renewable electricity, renewable gas, or electrify its heat demand or transition to electric vehicles.

Scope 3 emissions — This category encompasses all emissions linked not to the company directly, but rather those for which the organization bears indirect responsibility along its value chain. These emissions stem from various sources, such as purchasing products from suppliers and the emissions resulting from customers’ use of the company’s products. In terms of emissions, Scope 3 emissions account for the largest portion.

Companies will normally have the source data needed to convert direct purchases of gas and electricity into a value in tonnes of GHGs. This information may sit with procurement, finance, estate management, or in sustainability functions.

Scope 1 and 2 are most within an organisation’s control and in some cases the solution for net zero is available.

For numerous businesses, Scope 3 emissions make up more than 70 per cent of their total carbon footprint. Take, for instance, an organization involved in manufacturing products; substantial carbon emissions arise from the extraction, manufacturing, and processing of raw materials.

To address these emissions, you can consider collaborating with current suppliers to find solutions that reduce their impact or explore potential changes in your supply chain. However, it’s essential to recognize that suppliers also play a significant role in emission reduction through their own purchasing decisions and product design.

While defining what constitutes net-zero ambition can be complex, businesses striving for best practices will commit to addressing Scope 3 emissions in their plans. A great starting point is mapping your emissions footprint, analysing the scale and the degree of control you have over each source. Prioritizing emissions hotspots that are within your reach will be a practical approach to tackling them effectively.

Building blocks to achieving net-zero

The recent surge in corporate net zero commitments is a vital and promising development, but there is still much more to do. Out of the close to 300 companies with public net zero pledges today, many commitments remain vague in how value chain emissions will be tackled, and downstream emissions from products, services, and investments. These are the largest sources of emissions for most companies (referred to as Scope 3 emissions) and failure to address these emissions will fail to achieve a net zero economy. Furthermore, companies are still at the very early stages of embedding net zero into business and supply chain strategy and transformation efforts. As net-zero requires full value chain transformation, companies cannot act alone, and success will be dependent on a common and accelerated path forward.

Critically, the end goal is not just net zero, but a thriving, socially just, net zero future. Marginalised groups and low-income communities often bear the greatest impacts of climate change and there will be transitional implications for workers, sectors, communities, and regions that will need to be managed. Companies must help enable the conditions needed to achieve effective, just, and sustainable climate solutions for people of all gender, race, and skills. Examples include proactively driving inclusivity and social impact of new net zero products and solutions, upskilling and reskilling to enable an inclusive workforce transition, upskilling and broader support for SME partners and suppliers, integration of social metrics into reporting and disclosure around net zero, and incorporating inclusion and a “just transition” into policy advocacy efforts.

For companies to deliver their net zero commitments, they will need to undertake end-to-end business transformation. This includes understanding the implications of net zero for a company’s growth strategy and operating model and embedding net zero across all business functions from governance, to supply chains, to finance and innovation.

Building blocks for corporate net zero transformation. This ‘blueprint’ seeks to help companies move from willingness to implementation: This blog briefly defines the checklist of critical actions needed to undertake to transform to net zero and explains why these actions are important.

Building ambition – It’s of utmost importance to ensurethat your company has the intention of becoming carbon neutral and to make sure your net-zero targets are aligned with global ambition. The net-zero vision should set out timeframes and accountability, how the company intends to decarbonize emissions from its operations and value chain, its approach too hard to eliminate residual emissions through offsetting, and an enabling investment strategy.

Strategy across the supply chain – To achieve net-zero emissions, companies must develop a comprehensive strategy that addresses emissions throughout their entire supply chain. This means not only focusing on their direct operations (Scope 1 emissions) and energy consumption (Scope 2 emissions) but also tackling emissions associated with their suppliers, customers, and other partners. A well-defined strategy across the supply chain is important to identify and to help mitigate the largest sources of emissions ensuring a holistic approach to achieving net-zero.

Cost effective and sustainable innovation –Net-zero transformation requires innovative solutions that are both environmentally sustainable and economically viable. Companies need to invest in research and development to drive sustainable innovation, finding ways to reduce emissions without compromising the quality and competitiveness of their products and services. Embracing green technologies, renewable energy, and resource-efficient processes will be essential indriving meaningful progress towards the goal.

Engagement and transparent – Open communication and engagement with stakeholders are vital for successful net-zero implementation. Companies should involve employees, customers, investors, suppliers, and local communities in their net-zero journey. Transparent reporting on emissions reduction progress and sharing climate-related data will build trust and accountability. Moreover, engaging with external organizations and industry peers can foster collaboration and shared learning, accelerating the transition to a net-zero economy.

In house capability/ capacity – Achieving net-zero requires skilled professionals who can lead and execute the transformation initiatives effortlessly within the company. Building in-house capability and capacity through training and upskilling employees is crucial to drive change successfully. Companies should invest in developing expertise in sustainability, carbon accounting, and other relevant fields, enabling them to make informed decisions and implement sustainable practices across all business functions.

While these building blocks serve as a starting point for companies to begin their journey towards net-zero, it’s important to recognise that each company’s path will be unique. Flexibility, adaptability, and continuous improvement are essential as companies navigate the complexities of the net-zero transition. By taking decisive actions across their supply chain, fostering innovation, being transparent, and investing in their workforce, companies can contribute to a socially just, thriving, net-zero future for all.

Kenya’s domestic market is more than 56 million people and is considered one of East Africa’s core business and logistics hubs. Agriculture is the backbone of Kenya’s economy and central to the country’s development strategy. It accounts for 31.5% of Kenya’s GDP and employs 38% of the population.Despite this, food insecurity persists, with 4 million people facing extreme shortages during the 2022 drought. Limited access to markets and poor post-harvest practices contribute to 40% of food waste. The rising population, climate change, and disruptions in food supply chains pose further challenges, making an effective Cold Chain Infrastructure (CCI) crucial to mitigate many of these challenges.

A well-designed and developed cold chain can prevent food losses and reduce greenhouse gas (GHG) emissions related to food waste. Cold chains also ensure food security by reducing food price inflation, buffering the food supply, and overcoming seasonal shortfalls. This buffering mechanism dampens the price fluctuations that typically put vulnerable communities at risk of poverty and hunger and better supports the growth of farmers’ incomes.

Challenges faced by Kenya in growing CCI:

Limited technical skills to provide after-sales services.

Affordability – Cooling interventions need to be affordable and add value for farmers operating on thin margins. Usage-based payment models like CaaS, group ownership, and lease-to-own (PAYGO) can help reduce adoption barriers.

Consumer awareness: There is limited awareness, especially among rural smallholder farmers, of the benefits of using cold chain solutions.

Market dynamics and maturity: In Kenya, most food production is consumed within the country, and informal channels are common for selling products. For instance, over 99% of meat and 96% of fruits and vegetables are consumed locally through farmgate or domestic markets. Unlike export markets, domestic markets typically lack strict regulations and standards that require the use of a cold chain. While some players may use cold chain methods to extend produce shelf life, cooling is not mandatory.

Lack of investment: Access to affordable debt and equity for service providers is needed, but the sector is still relatively young, and the financial needs are diverse. More established companies are ready for long-term patient capital and concessional loans. However, there is still a need for grants and programme support for market development activities

Weak transportation infrastructure: Poor road conditions and traffic congestion increase travel time and increase the risk of perishable products becoming damaged and spoiled. In addition, poor roads and infrastructure can damage refrigerated trucks/vehicles, resulting in the leakage of high GWP refrigerants

Inconsistent policies: Tariff regimes are inconsistent, and agro-based products have a favourable import duty, but it’s unclear if this is applicable to all value chains (e.g., meat and fish) and for components. The lack of national standards for energy performance and food quality also inhibits market growth

Availability of equipment and suppliers: The development of a clean cold chain will have to be preceded by policies that encourage the import of cold-chain equipment in the country by local firms or even incentivise foreign firms to set up subsidiaries. That means that an entire industry will have to be developed or at least nurtured, including local manufacturers being encouraged/incentivised to undertake production.

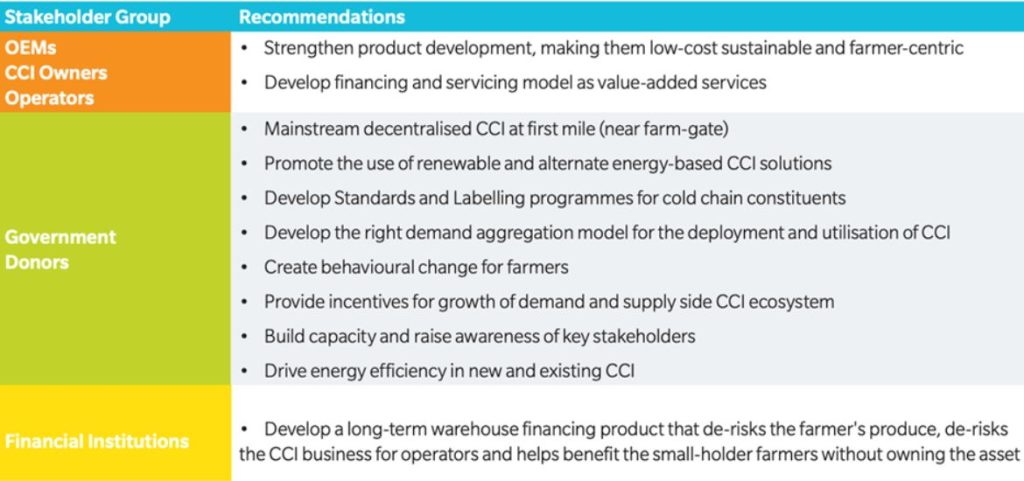

Key recommendations for carious stakeholder Groups in Kenya’s CCI Sector

xr:d:DAFvn3wv324:2,j:29677603515831815,t:23092707

Challenges that Inhibit the Uptake of CCI Solutions

Several factors inhibit the adoption of CCI technologies on the side of both users and manufacturers. These challenges are as follows:

Financing challenges: Financing is challenging for enterprises/service providers and consumers/beneficiaries. Limited financing is available to enterprises creating and providing CCI, as well as to end consumers looking to acquire these technologies

Technological challenges: While technological innovation has been seen in the CCI sector, several challenges still exist. These include the availability of technicians required to manage installation and after-sales services, both critical to adopting new technologies. Meanwhile, poor-quality products negatively impact how customers view the entire sector, while limited local manufacturing capacity hinders local job creation and leads to import substitution.

Market and operational challenges: These include policy gaps regarding supply-side and demand-side incentives at the national and county levels. The immaturity of the market limits economies of scale regarding sector consolidation, bulk procurement, and the ability of individual companies to absorb commercial funding. As a result, most value chains remain primarily informal.

User challenges: The most common user-related challenge is limited familiarity with CCI solutions, including key product features like energy efficiency, usage and maintenance, and temperature control. Since most smallholder farmers are rain-dependent, the seasonality of their produce also impacts the utilisation rates of CCI assets, especially those using CaaS models. This has long-term impacts on technology providers’ margins, leading to more extended payback periods.

Potential Interventions to Increase the Uptake of CCI Solutions

Various strategies could be adopted to increase the uptake of CCI solutions in the country and to ensure they scale by 2030. Some of these strategies are as follows:

Increase patient capital in the sector: To promote CCI adoption, the sector requires more patient and catalytic capital, including long-term equity from commercial investors and grant financing. Targeted recipients are companies involved in CCI solutions and MFIs providing consumer financing for farmers.

A first loss default guarantee programme in which a donor agrees to deploy grant capital as part of the investment to reduce losses in case the ROI is negative, thus catalysing participation from more commercial co-investors.

Results-based or performance-based financing, where an investor or financier provides patient capital to achieve measurable impact; this could be the amount of food the CCI solution “saves” from wastage.

Public Private Partnerships (PPPs) include a mechanism whereby the government provides financing for an asset while the private sector player is responsible for its repair, maintenance, and the technical support required to ensure sustainability.

Re-evaluate the tax regime and reduce prices: The tax regime for CCI parts and components significantly raises their prices, accounting for almost 40% of production costs. This high cost hinders CCI adoption, particularly at the initial stage. Re-evaluating the tax system is crucial, and efforts should be made to provide tax subsidies through multistakeholder taskforces. This will lead to more affordable CCI solutions, incentivizing their uptake in the market.

Increase donor programmes that promote market development activities: Increase donor-sponsored programs to promote market development of CCI assets. Focus on building technical skills, local manufacturing, and after-sales services. Educate farmers and consumers to boost adoption. Fund successful pilots to reduce risk perception among stakeholders.

Increase processing and exports: To promote CCI technologies, Kenya should focus on increasing local food processing and exports, while adhering to Global Agricultural Practices, including cold chain requirements, to meet quality standards for export markets.

To promote CCI technologies, Kenya needs dedicated policy support and full implementation. Specific regulations can cover optimum produce temperature, pricing, and certified technical providers. Publicly funded capacity building for cooling engineers can enhance skills. Tailored recommendations for different markets can further boost CCI adoption.

For the household refrigerator market:

Resolve PAYG compatibility, appropriate system controls and improved reliability.

Develop financing solutions through micro-finance and PAYG contracts in mini-grid markets.

Provide after-sales technical support and the means to deliver appliances to remote regions.

For the small commercial refrigerator market:

Encourage development of appliances for target markets and collaborate with regional business associations and SACCOs.

Design “solar stalls,” soft drink coolers, and portable coolers for farmers and producers, emphasizing reliability.

Develop financial case templates and suitable financing packages for entrepreneurs.

Ensure after-sales technical support for sustained operations.

For the commercial ice-maker market:

Encourage targeted appliance development and collaboration with farmers’ cooperatives.

Focus on small agricultural, meat, fish, and dairy storage and transportation systems.

Provide financial case templates and suitable financing options.

Establish after-sales technical support.

Although use cases vary across value chains, overall, CCI in Kenya is underdeveloped in the agricultural sector, resulting in significant quantities of food lost yearly due to a lack of cold chain technology. CCI manufacturers and distributors must ensure that their products correspond to the needs and capacities of the first-mile market segment, particularly concerning the power sources they use and the payment models they adopt. In supporting innovations in cold chain technology, there should be a particular focus on products powered by renewable energy.

However, solving this problem requires more than the proper technology; a system-wide approach combining education, financing, and policy changes is needed to fully realise the cold chain market’s potential and for Kenyans to reap its benefits eventually.

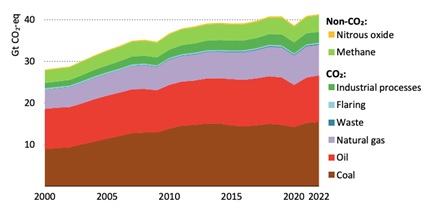

Global energy-related greenhouse gas (GHG) emissions remain a significant threat to the climate due to their due to their magnitude and longevity. As per International Energy Agency (IEA) analysis[1], the total energy emissions increased to an all-time high of 41.3 Gt CO2-eq as shown in Figure 1.

Figure 1. Global Energy GHG Emissions

The emissions from energy combustion and industrial processes accounted for nearly 89% of emissions in 2022.Additionally, methane emissions from energy combustion, leaks and venting contributed another10%. These emissions present a stark picture of the climate change situation, as evidenced by recent extreme weather events observed worldwide (e.g., heat waves, floods, droughts, wildfires, etc.).According to the IEA’s World Energy Outlook 2022 analysis[1], global greenhouse gas (GHG) emissions are on track for a significant increase if investments in climate change mitigation are reduced and strict policies are not implemented. The projections indicate that energy related GHG emissions could surpass 55 GtCO2-eqby 2050.

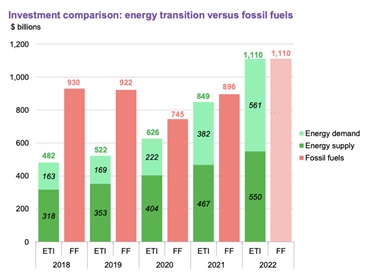

This situation underscores the pressing need for immediate investment in energy transition technologies, encompassing both the supply side (renewable energy, nuclear power, energy storage, hydrogen, etc.) and the demand side (e-mobility, electrified heat, etc.). Historically, countries have predominantly directed significant investments towards fossil fuels to bolster energy security. However, energy transition investments matched fossil fuel investments for the first time in 2022, reaching USD 1.1 trillion, as depicted in theFigure 2. This represents a notable increase of USD 261 billion from the previous year.The shift in investment towards cleanenergy is a historic change that is unlikelyto be reversed, as low-carbon industriescontinue to grow.

Figure 2. Investment Comparison: Energy Transition (ETI) vs. Fossil Fuels (FF)

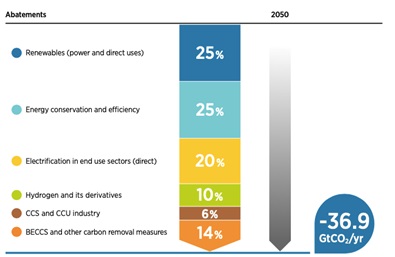

Figure 3. Energy CO2Emission Reductions by 2050 in 1.5°C Scenario

It is important to note that the current investment levels, although encouraging, are insufficient to propel towards the ambitious goals of1.5°C pathway.To set a course on a 1.5°C pathway, the energy transition urgently needs to accelerate; therefore, a holistic, multi-faceted approach is necessary.International Renewable Energy Agency (IRENA) analysis shows that a combination of renewables (both power and end use, electrification and fuels such as hydrogen) and energy efficiency, can provide 80% of the CO2 reductions needed to align the world on a 1.5°C pathway, as shown in Figure 3.To achieve this target, it is estimated that an annual average investment of USD 4.4 trillion will be required, which is equivalent to about 5% of global gross domestic product (GDP).

Potential sources of this funds

Climate finance investments have seen contributions from both public and private sources. Public sources, such as governments themselves; a combination of national Development Financial Institutions (DFIs), multilateral and bilateral DFIs; state-owned financial institutions; and others have played a significant role by providing grants and debt financing. Similarly, private sources, including commercial banks and corporations, have been at the forefront of financing climate-related initiatives. Some of the potential sources are explained below:

Many governments are establishing the banks as National Development Financial Institutions (DFIs) that focuses on raising and investing fundsacross different industry sectors of the country. This is becoming governments most important financial institution to support and mobilise capital to develop productive investments. Many countries like Germany (kfW), Singapore (DBS), Brazil (BNDES), India (SIDBI), South Africa (DBSA), etc. has their own DFIs established and are promoting and supports the development of innovation, a green economy and sustainable projects.

Green Bondsare a form of debt instrument and were developed in 2008 in response to growing concern about climate change and sustainability. When an entity issues a green bond, it is essentially borrowing money from investors who purchase the bond. The issuer agrees to pay back the principal amount of the bond along with periodic interest payments over a specified period of time.As of January 2023, green bonds have raised $2.5 trillion globally[1] to support green and sustainable projects.The World Bank, known for issuing the inaugural green bond in 2008, has continued its leadership in this field. To date, they have issued over 200 green bonds in 25 currencies, making significant contributions to the development of sustainable finance. Their efforts have also resulted in the establishment of the Green Bond Principles (GBP), which have emerged as international best practices for transparency and disclosure in the green bond market. [4]Low-cost Finance for the Energy Transition, IRENA 2023

International financial entities likeGlobal Environment Facility (GEF), Green Climate Fund (GCF), etc.have a primary goal of providing support for global environmental and climate-related projects. These entities place a strong emphasis on country ownership and alignment with national priorities and plans. They support projects and programs that include technical assistance and investments (typically for pilot implementation), which are in line with recipient countries’ national climate strategies and objectives. These funds are intended to mobilize additional resources and leverage investments from various stakeholders within the respective countries. So far, the GEF has disbursed over $22 billion in grants and blended finance, while also mobilizing an additional $120 billion in co-financing for over 5,000 national and regional projects[2]. Likewise, GCF has raised USD 10.3 billion equivalent as of July 2020[3].

Innovative financing tools such ‘debt-for-climate-swaps’ in which international creditors will agree to reduce debt, either by converting it into local currency, lowering the interest rate, writing off some of the debt, or through a combination of all three. The debtor will then redirect the saved money towards initiatives aimed at increasing climate resilience, lowering GHG emissions or others.

The expansion of blended finance refers to the increasing use and promotion of innovative financing mechanisms that combine public and private resources to address development challenges and mobilize additional investment. It can play an important role in derisking investments, attracting private capital, etc. to projects and initiatives that contribute to sustainable development.Public resources alone are often insufficient to address the vast financing needs required for sustainable development. By blending public and private resources, governments, development finance institutions, and other stakeholders can leverage the strengths of both sectors.

The above discussion highlights the importance of investments in energy transition technologies. Countries need to not only increase their own investments but also facilitate greater financing in developing and emerging economies. It is essential to recognize that relying on just a few financing solutions will not be sufficient. Instead, countries must explore multiple financing options to create economies of scale for emerging energy transition technologies.

The development of cold chain infrastructure is crucial for a country like India, which has a large agricultural sector and a significant need for efficient storage and transportation of perishable goods such as fruits, vegetables, dairy products, and pharmaceuticals. Government policies and initiatives play a key role in the large-scale development of cold chain infrastructure in India. The Indian government recognizes the importance of cold chain infrastructure and has implemented various policies and initiatives to promote its large-scale development.

One of the key approaches taken by the Indian government is the introduction of subsidies and grants-in-aid to incentivize the establishment of cold chain facilities. These financial incentives aim to offset the high capital costs involved in setting up cold storage units, refrigerated transportation, and other infrastructure components. The subsidies help reduce the financial burden on entrepreneurs and encourage private sector participation in cold chain development.

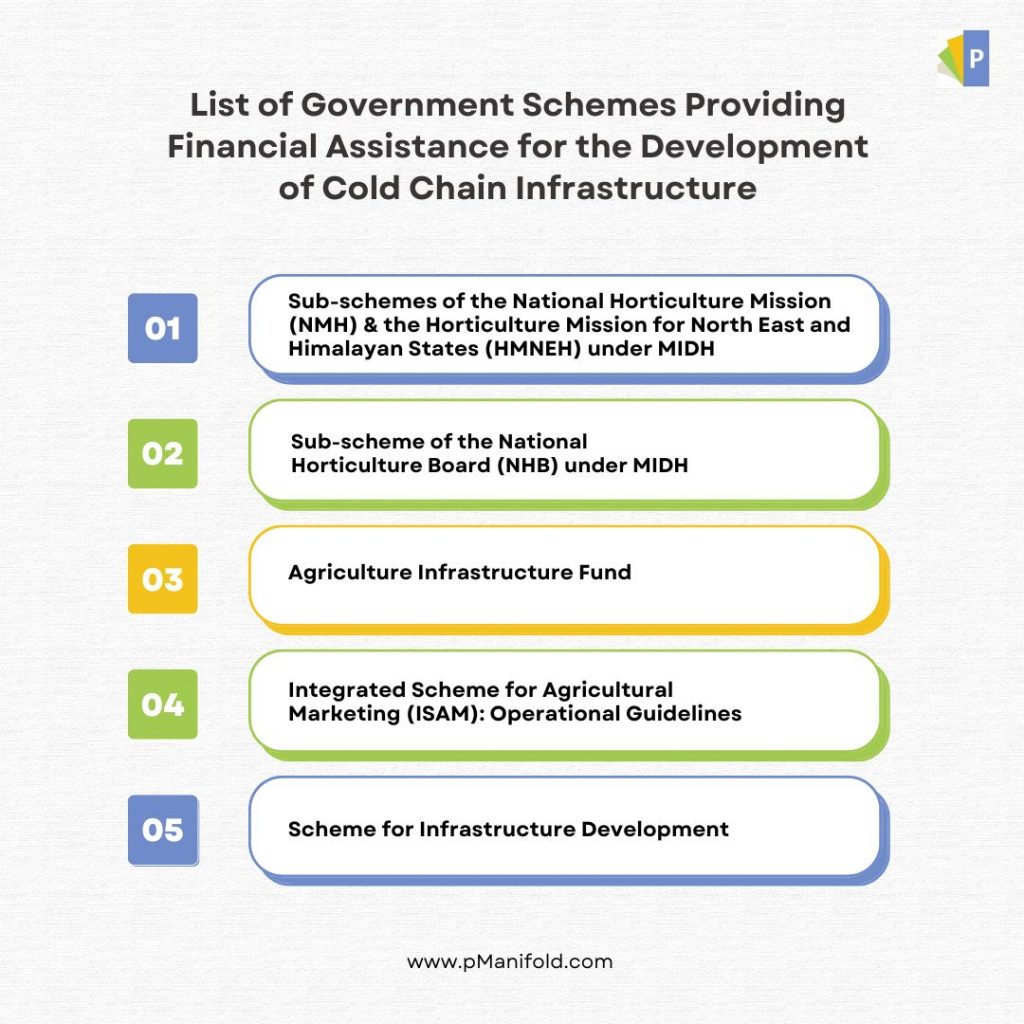

These flagship programmes promote the development of complete end-to-end cold chains, from the source to the end-customer. These initiatives aim to bridge the gaps in the existing supply chain and ensure the seamless movement of perishable goods. Some of these programs include:

Mission for Integrated Development of Horticulture (MIDH)

MIDH is a government scheme for holistic growth of the horticulture sector ((fruits, vegetables, root and tuber crops, mushrooms, spices, flowers, aromatic plants, coconuts, cashews, cocoa and bamboo shoots). It provides financial assistance, including for cold storage. Subsidies of 35% (or 50% in hilly areas) are available. MIDH helps establish energy-efficient multi-chamber cold storage units with thermal insulation, humidity control, advanced cooling systems, and automation. Long-term storage hubs up to 5,000 MT capacity are covered by NHM/HMNEH, while 5,000-10,000 MT hubs are covered by NHB scheme.

National Horticulture Mission (NHM) / Horticulture Mission for North East and Himalayan States (HMNEH)

Long-term cold storage and distribution hubs of up to 5,000 MT capacity are eligible for assistance under this open-ended sub-scheme of MIDH. Assistance comes in the form of credit linked subsidies, amounting to 35% of the capital cost of the project, or 50% in NE, hilly and Scheduled Areas.

National Horticulture Board (NHB)

The National Horticulture Board (NHB) is implementing the “Capital Investment Subsidy for Construction/Expansion/ Modernisation of Cold Storages and Storages for Horticulture Products.” Under this scheme (a sub-scheme of MIDH), assistance is available for the installation and modernization of cold storage units with capacity between 5,000 MT and 10,000 MT. This is an open-ended credit-linked programme offering subsidies amounting to 40% of the capital cost of a project (limited to INR 30 lakhs per project), or 50% in NE, hilly areas and Scheduled Areas (limited to INR 37.50 lakhs per project) sub-scheme of MIDH. Assistance comes in the form of credit-linked subsidies amounting to 35% of the capital cost of the project, or 50% in NE, hilly and Scheduled Areas.

Pradhan Mantri Kisan SAMPADA Yojana (PMKSY)

SAMPADA stands for Scheme for Agro-Marine Processing and Development of Agro-Processing Clusters. It consists of a comprehensive package to create modern infrastructure and efficient supply chain management from farmgate to retail outlet, with the goal of boosting the growth of the food processing sector and improving returns for farmers. This is in line with the GoI’s goal to double farmers’ income, creating significant employment opportunities in rural areas. It also reduces food waste, using efficient and modern technology to help the food processing industry and export houses convert surplus produce into an export commodity.

The following will be developed under PMKSY:

Mega Food Parks

Integrated cold chain and value addition infrastructure

Creation, expansion and modernization of food processing and preservation capacities

Infrastructure for agro-processing clusters

Backward and forward linkages

Food safety and quality assurance infrastructure

Human resources and institutions

So far, the Ministry has approved 41 Mega Food Parks, 353 cold chain projects, 63 agro-processing clusters, 292 food processing units, 63 backward and forward linkages projects and 6 Operation Green projects across the country.

Scheme for Integrated Cold Chain, Value Addition and Preservation Infrastructure

Part of PMKSY, this scheme is implemented by the Ministry of Food Processing Industries (MOFPI) with the aim of reducing post-harvest produce losses and providing better prices to farmers for their produce. Financial assistance (grants-in aid) is limited to a maximum of INR 10 crore per project for technical civil works, eligible plants and machinery, subject to the following conditions:

For storage infrastructure (including packhouses, pre-cooling units, ripening chambers and transport infrastructure), grants-in-aid are provided amounting to 35% of total project cost, or 50% for NE and Himalayan States, Integrated Tribal Development Project (ITDP) Areas and islands.

For value addition and processing infrastructure (including frozen storage and deep freezers integral to processing), grants-in-aid are provided amounting to 50%, or 75% for NE and Himalayan States, ITDP Areas and islands.

For irradiation facilities, grants-in-aid are provided amounting to 50%, or 75% for NE and Himalayan States, ITDP Areas and islands.

For reefer vehicles, credit-linked back-ended grants-in-aid are provided amounting to 50% of the cost of a new reefer vehicle/mobile pre-cooling van, up to a maximum of INR. 50.00 lakh. Integrated cold chain and preservation infrastructure can be set up by individuals, groups of entrepreneurs, cooperative societies, Self Help Groups (SHGs), Farmer Producer Organisations (FPOs), NGOs or central/state PSUs. Standalone cold storage units are not covered under the scheme.

Small Farmer Agri-Business Consortium (SFAC) Assistance

These subsidies are available for cold storage facilities set up as part of an integrated value chain project, provided the cold storage component accounts for no more than 75% of the Total Financial Outlay (TFO). Subsidies can amount to 25% of the capital cost of a project with a maximum ceiling of INR 2.25 crores, or 33.33% with a ceiling up to INR 4 crores in NE, hilly and Scheduled Areas.

In order to meet the government’s goal of doubling farmers’ income by 2022, several market reforms are being rolled out to encourage the development of CCI:

The establishment of 22,000 Gramin Agriculture Markets (GrAMs) to act as aggregation platforms

An Agri-Export Policy, which aims to double agri-exports by 2022

The promotion of 10,000 FPOs by 2024

The creation of the following Corpus Funds:

An agri-marketing fund to strengthen eNAM6 and GrAMs (INR. 2,000 crores)

An Agricultural Infrastructure Fund (AIF) to provide collateral-free loans with an interest subvention of 3% (INR. 100,000 crores)

Apart from this, the government is also providing profit-linked tax holidays, priority sector lending, and lower tax rates for raw and processed products. Cold chain services – including pre-conditioning, pre-cooling, ripening, waxing and retail packing – are also exempt from Goods and Service Tax (GST).

Some of the other key government initiatives in the cold chain sector are as follows:

Exemption from Customs and Excise Duty

Customs Duty: A concessional basic customs duty (BCD) of only 5% is applied for cold storage, cold room and industrial projects (including farm-level precooling) for the preservation, storage or processing of agricultural, horticultural, dairy, poultry, aquatic and marine produce and meat. Truck refrigeration units and other refrigerated vehicles are fully exempted from BCD.

Excise Duty: Central excise duty has been fully exempted for the installation of cold storage, cold rooms and refrigerated vehicles for the preservation, storage, transport and processing of agricultural, apiary, horticultural, dairy, poultry, aquatic and marine produce and meat. This also applies to air conditioning equipment and refrigeration panels for cold chain infrastructure, including conveyor belts used in cold storage units, mandis and warehouses.

Foreign Direct Investment (FDI):

100% FDI is allowed, leading to an increase in private sector investment. This policy requires a minimum investment of US$100, with at least 50% invested in back-end infrastructure.

Fiscal Incentives for Cold Chain”

Section 80-IB of the Income Tax Act provides deductions for cold chain-related industrial activity. Deductions apply to 100% of profits for the first five years, then 25-30% for the next five years.

Under Section 35-AD of the Income Tax Act 1961, deductions of 150% are permitted for expenditure incurred in setting up a cold chain facility.

These government initiatives aim to reduce post-harvest losses, improve farmers’ income, create employment opportunities, and enhance the overall efficiency of the agricultural supply chain.

GOI’s schemes and initiatives to support cold chain infrastructure signify its commitment to fostering efficient storage and transportation of perishable goods. By providing subsidies, grants, and incentives, the government encourages private sector participation, reduces post-harvest losses, and promotes the overall growth of the agricultural sector. These efforts align with broader goals of doubling farmers’ income, boosting food processing, and enhancing the efficiency of the supply chain. Overall, the government’s focus on cold chain development contributes to the economic growth and sustainability of India’s agricultural industry.

List of Government Schemes Providing Financial Assistance for CCI Development

Every year due to post-harvest losses, US$19.4 million worth of crops are wasted in India daily due to rejection at the farmgate and delays in the distribution process with significant impacts on the environment. Effective Cold Chain Infrastructure (CCI) is one intervention that could mitigate many of these challenges.

India is the world’s highest milk producer and the second-largest food producer. Agriculture, alongside its associated sectors, is India’s largest source of livelihood.

Almost 70% of rural households depend primarily on agriculture, and 86% of farmers are smallholders. Despite this production level, India is still home to over 190 million malnourished people, a quarter of the world’s total. The Global Hunger Index 2020 report ranks India 94th out of 107, lagging behind neighbouring countries like Bangladesh, Pakistan and Nepal. Farmers and food producers, especially smallholder farmers, still struggle with low-income levels, and 4.6-15.9% of fruits and vegetables (FFV) are lost annually throughout the supply chain. The country loses approximately INR 926 billion (US$14.33 billion) every year due to post-harvest losses, and US$19.4 million worth of crops are wasted in India daily due to rejection at the farmgate and delays in the distribution process with significant impacts on the environment in terms of toxic waste, water pollution, long-term damage to ecosystems, hazardous air emissions, greenhouse gas emissions and excessive energy use. Effective Cold Chain Infrastructure (CCI) is one intervention that could mitigate many of these challenges.

As the world’s second largest food producer, India should be able to feed its population; instead, 190 million Indians are malnourished. Proper food preservation techniques could help change this by ensuring that a higher proportion of domestically produced food reaches the Indian population. Reducing food losses would also boost the incomes of smallholder farmers and others who earn their livelihoods at the first mile segment of the value chain, creating jobs and improving food security for rural populations.

What is a cold chain?

A cold chain is an environmentally controlled chain of logistics activities that cools and preserves produce or products within stipulated parameters, including temperature, humidity, atmosphere, and packaging. A well-designed and developed cold chain can prevent food losses and reduce carbon emissions related to food waste. Cold chains also ensure food security by reducing food price inflation, buffering the food supply, and overcoming seasonal shortfalls. This buffering mechanism dampens the price fluctuations that typically put vulnerable communities at risk of poverty and hunger and better supports the growth of farmers’ incomes.

Barriers to Scaling-up CCI Business Models:

Different stakeholders in the cold chain sector face economic barriers that need to be addressed through a sustainable business model. These barriers include:

High investment cost:

Large-capacity CCI requires a sizable investment. For example, a 5,000 MT cold storage facility costs around INR 5-6 crore (US$670,000-800,000), including the cost of the land. A reefer truck with a 7.2T capacity costs around INR 18-19 lakh (US$24,000). Although the government provides subsidies of 35-75%, the remaining cost is still too high for most farmers.xxiii

High cost of land and its availability to the operator or service provider:

The cold chain business is capital intensive, and installing high capacity (~5,000 MT) cold chain infrastructure (like packhouses and cold storage facilities) becomes even more expensive due to the high cost of land. To access government subsidies the land where the cold storage unit will be installed must be owned by the individual or company, and a 5,000 MT-capacity cold storage unit requires 1-2 acres of land. Securing land near a farmgate can also be challenging for OEMs and operators.

High operating costs:

Most rural areas have access to grid electricity, but it is highly unreliable. This is a major issue for CCI near a farmgate, because it requires a constant power supply. Operators are forced to rely on diesel generators for about 30% of total expenses for the cold storage industry in India.

Access to financing:

Access to financing is a challenge for smallholder farmers. Low-income earners, many of whom are unbanked and have little financial literacy, find it extremely difficult to secure loans to purchase a cold storage facility since they are considered a credit risk. Loans and subsidies are generally only available to government institutions and FPOs, not to individual farmers.

Demand aggregation:

Due to a lack of awareness of the benefits of cooling, demand aggregation is often a challenge for CCI operators, resulting in low utilisation rates.

Low utilisation affecting revenue:

Low utilisation rates are a major challenge to the business viability of CCI. 90-95% of CCI assets are owned by the private sector, but due to smallholder farmers’ limited ability to pay for storage and transportation, many do not use the cold storage available. CCI funded by the government also lacks modern efficient technology and transport facilities, resulting in low capacity and utilisation. To ensure better adoption of CCI, it is important to develop sustainable and affordable business models for farmers. The focus should be on decentralising CCI solutions, which would reduce investment costs. Decentralisation would also make CCI more accessible to farmers and increase utilisation of the assets, resulting in better revenues for operators and allowing farmers to sell their produce at relatively high prices. The pay-as-you-store model should be scaled up, since it lifts the burden of ownership from the farmer and therefore removes the barrier of financing.

Also read : Challenges to the Uptake Of CCI

Potential Interventions to Increase the Uptake of CCI

Various strategies could be adopted to increase the uptake of CCI solutions in India, and to ensure that these solutions scale by 2030. The following are some recommendations for the sector.

For the Government and Donors:

Mainstream decentralised CCI at first mile (near farmgate):

Most CCI today are centralised and high-capacity, located near urban areas which are expensive for farmers (especially smallholder farmers), and are difficult to access. Decentralising CCI can potentially solve the problem of access, benefiting farmers from cold storage through improved incomes. Decentralised CCI solutions would also significantly reduce post-harvest losses, since unsold produce could be stored rather than being discarded or spoiling. Such units could provide multi-commodity storage at affordable rates near the farmgate. The government should consider scaling them up through a programmatic intervention similar to the KUSUM scheme, which focused on solar water pumps (SWPs).

Promote the use of renewable and alternative energy-based CCI solutions:

The government should promote the use of off-grid solar PV for CCI technology, as well as solar thermal systems, solar-biomass hybrid systems and PCM for thermal storage. There are several different ways this could be done: providing additional incentives for renewable energy-based CCI solutions under existing subsidy schemes; integrating support for CCI into existing renewable energy schemes (such as the SWP KUSUM Scheme, since the excess power generated by SWP systems could be used to power small cold rooms near the farmgate); or promoting the Decentralised Renewable Energy livelihood scheme. Deployment of these technologies would both reduce GHG emissions and mitigate the risks associated with weak grid connectivity. It could also bring down operating costs significantly, making CCI less expensive for operators and allowing farmers to store their produce at more affordable rates.

Develop a standards and labelling programme for cold chain components:

Decentralized renewable CCI solutions should have defined and measured energy efficiency, quality, and performance. The Bureau of Energy Efficiency (BEE) under the Ministry of Power (MoP) can establish energy performance parameters and minimum standards (MEPS) for equipment and appliances. BEE’s Standards and Labelling (S&L) program, which has improved energy efficiency for various consumer products, could be extended to cold chain technologies. Technical specifications and cost benchmarks for renewable-based CCI solutions are currently lacking, leading to improperly sized systems. Clear standards and guidelines would promote technology innovation and help consumers choose the best options.

Develop demand aggregation models for deployment and utilisation of CCI:

Today, CCI is concentrated in urban areas, primarily consisting of high-capacity and capital-intensive cold storage facilities. This uneven distribution leads to operational inefficiencies, undermining the benefits of the cold chain. The high investment costs hinder CCI growth, and low demand aggregation results in underutilised assets and increased costs for farmers. To address these issues, demand aggregation is necessary to deploy appropriately sized and technologically advanced CCI across the cold chain while reducing upfront expenses. This can be achieved through data-driven optimization of overall cold chain requirements and integrated deployment of storage and transport facilities. Establishing a feedback loop from wholesalers, retailers, and consumers to producers enhances farmers’ decision-making, amplifying the holistic benefits of CCI. A demand aggregation model similar to the successful programs for LED bulbs and electric vehicles, implemented by Energy Efficiency Services Limited (EESL), can lower upfront costs. Such a model could be integrated into existing government schemes like KUSUM, utilising surplus power from solar water pumps for productive-use applications.

Create behavioural change for farmers:

There is a need to provide incentives for medium and smallholder farmers to start using CCI. Stakeholders report a lack of awareness around CCI among farmers, who see it as a luxury rather than a necessity. Enhanced understanding of cold chain technology should change this perception, driving CCI uptake and improving income generation opportunities for farmers. Awareness drives led by government, financing institutions like NABARD, and NGOs would demonstrate the benefits of using CCI, convincing farmers to adopt it. Such campaigns could educate farming communities on pre- and post-harvest cooling practices to better manage their produce, and on how cold chains can improve incomes. This could be done through targeted consumer campaigns such as mobile van displays, live demonstrations and goodwill ambassadors, all of which will help scale demand for CCI.

Provide incentives for demand and supply side CCI ecosystems:

Currently, the government is providing various capital subsidies for CCI development. It is recommended that the government uses additional incentives to encourage the growth of both a demand side and a supply side CCI ecosystem. The supply can be boosted through grants, tax rebates and R&D funds, while providing fiscal incentives to CCI users would help grow demand. The supply side ecosystem could also be developed through capacity building, creating a pool of service providers and technicians. This would not only grow the CCI industry, but would establish India as a leader in CCI for both domestic use and export.

Build capacity and raise awareness of CCI:

Lack of awareness hampers the optimal operation of CCI, impacting commodity quality and consumer confidence. To address this, comprehensive capacity building and training are needed throughout the supply chain, including farmers, operators, and technicians. Training should cover economic impacts, business models, technical expertise (such as temperature requirements), system monitoring, installation, and maintenance. Special focus should be given to empowering rural women through skill development programs like “Pradhan Mantri Kaushal Vikas Yojana.” Collaboration among industry leaders, associations like ISHRAE, practitioners, construction professionals, academics, NGOs, and CSOs is vital for developing effective training programs at grassroots level.

Drive energy efficiency in new and existing CCI:

The government should promote retrofits and replacement of existing inefficient CCI technologies, and the efficiency of new installations should be driven by the S&L programme. This would significantly reduce operating costs of CCI, and these savings can be passed on to the end-user in the form of affordable storage rates. EESL ran a similar Demand Side Management (DSM) programme to replace inefficient motors and air conditioning units. India currently has the world’s largest capacity of cold storage warehouses, but these are designed almost exclusively for the long-term storage of potatoes; this existing single-commodity CCI storage needs to be converted or retrofitted to store multiple commodities through preferred lending programmes.

For OEMs /CCI Owners /Operators:

Strengthen product development:

OEMs should focus on product development to make their products more low cost sustainable and farmer-centric. Using clean technology (refrigerants with low GWP) would make CCI solutions more climate friendly, which would be a better fit for the market. 2. Develop financing and servicing models: TOEMs and system integrators should leverage available government subsidies to provide end-to-end financing solutions for their customers; this includes exploring pay-as-you-store and Cooling-as-a-Service models. These models can be beneficial for smallholder farmers, who do not then need to own CCI themselves. OEMs should also focus on value-added features like warehouse financing products, after-sales support from trained personnel, and integration with reefer transport to improve market linkages

For Financing Institutions (FIs):

Develop a long-term warehouse financing product:

There is a need for a long term (10-15 years) financing product that de-risks farmers’ production, de-risks the CCI business for operators, and benefits smallholder farmers without requiring them to own the asset. This could be developed based on the business model of the FPO, especially those using the CCI for their own consumption or to build a new business as aggregators. For FPOs in tribal communities where this business is still nascent, longer term financing is critical. In order to reach last mile FPOs, farmers and aggregators, FIs would need to create awareness of the credit linkages and subsidies available for this sort of infrastructure (through the AIF and MIDH, for example), and would have to assist with the process of applying for these schemes and financial products. This could be done through NABARD, SFAC and other FIs empanelled under schemes like AIF.

Also read : Government Support for the Growth Of CCI

Although use cases vary across value chains, overall, CCI India is underdeveloped in the agricultural sector, and significant quantities of food are lost each year due to a lack of cold chain technology. Many smallholder farmers are still unaware of proper post-harvest handling procedures, and cannot access or afford the CCI they need to prevent losses. Business models like pay-as-you-store would help drive CCI uptake at the first mile level, as would farmer education and the development of more off-grid cold chain solutions that could reduce the risk of power cuts in areas with poor grid connectivity. Solving this problem requires more than the proper technology; a system-wide approach combining education, financing and policy changes is needed for the potential of the cold chain market to be fully realised, and for Indians to finally revolutionise their agricultural sector.

Read full assessment report on cold chain markets in India here

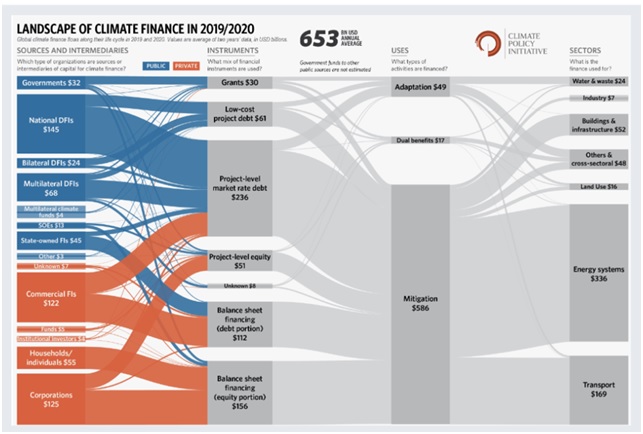

Climate finance refers to the financing needed to address the causes and impacts of climate change, including mitigation (reducing greenhouse gas or GHG emissions) and adaptation (managing the risks and impacts of climate change). The need for climate finance has grown as the world recognizes the urgent need to address the impacts of climate change, which are already being felt in many parts of the world. It has been steadily increasing over the past decade and reached USD 653 billion in 2019/2020.Figure 1shows how this finance is sourced (public or private) and used across six sectors:

i) water & wastewater;

ii) infrastructure & industry;

iii) land use;

iv) transport;

v) energy systems; and

vi) other & cross-sectoral.

Figure 1represents an average annual amount in USD billion for 2019 and 2020, and they provide an in-depth look at how funding is allocated throughout the lifecycle of climate projects. Some of the key observations are as follows:

The public sector provided USD 334 billion (51%), primarily through Development Finance Institutions (DFIs). Private actors contributed USD 319 billion (49%), with commercial financial institutions and corporations contributing almost 80%.

Grants made up 4.5% (USD 30 billion) of climate finance, with governments as the main source

Most climate finance raised was in the form of debt, with market-rate debt accounting for 88%, while low-cost debt was only 12%

Equity investments contributed 31% (USD 207 billion) of total climate finance

Around 90% of climate finance was for mitigation and adaptation finance accounted for 7% of total finance, while dual-use projects accounted for 3%

The majority of mitigation funding was allocated to energy systems, which included renewable fuel production, power and heat generation, transmission and distribution networks, policy support, and capacity building

The transport sector ranked second among sectors receiving climate finance, covering various modes such as EVs, rail & public transport, waterways, aviation, and transport-oriented infrastructure

Figure 1. Global Climate Finance Landscape

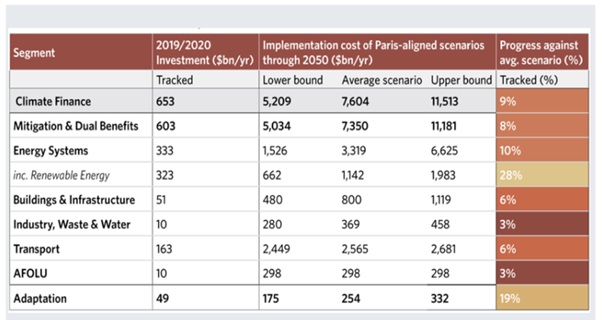

Figure 2. Climate Finance Comparison with Paris Scenarios

Although climate financing has been growing in recent years, it remains insufficient to meet the investment requirements for realizing Paris-aligned scenarios and achieving net-zero emissions by 2050.According to Figure 2,the amount of climate finance in 2019/2020 accounted only for approximately 9% of the average scenario implementation cost. A significant portion of these investments were directed towards climate mitigation efforts in the energy sector, with only 6% of the investment going towards the transport sector. The several challenges/ barriers hindering the financing and development of green projects are

i) lack of suitable financial instruments and long disbursement procedures ii) high perceived risk and initial investments required iii) limited technical capacity of stakeholders to develop green projects iv) inadequate understanding and use of low-carbon technologies v) lack of supportive regulatory conditions to drive green investments and others.

This disparity underlines the pressing need for a substantial increase in climate financing to align with net-zero targets. Without sufficient financing, it will be difficult to meet the goals of the Paris Agreement and prevent catastrophic consequences.

In order to successfully transition to a sustainable, net zero emissions, and resilient world within this decade, a significant increase in climate investment is imperative. Unfortunately, as depicted in Figure 3, current finance flows are vastly insufficient and fall far short of the estimated annual investment needs, which are projected to be in the range of $2-2.8 trillion by 2030. Investing in the energy system is crucial for addressing climate change, and prioritizing investments in the power and transport sectors makes sense given their significant contribution to greenhouse gas emissions. In the power sector, investments can be directed towards developing renewable energy sources such as solar, wind, hydro, and others. This will reduce reliance on fossil fuels and decrease carbon emissions. Additionally, investments can be made in energy storage technologies to ensure the stability and reliability of the power grid. In the transport sector, investments can be focused on developing electric vehicles and the necessary charging infrastructure. This will reduce reliance on fossil-fuel powered vehicles and decrease carbon emissions from the transportation sector. Additionally, investments can be made in public transportation systems to encourage the use of mass transit and reduce the number of individual vehicles on the road.

Figure 3. Climate Finance Investment Needs by 2030

Climate finance must increase in speed and scale this decade for a credible transition to a sustainable, net zero, and resilient world. It should count in the trillions annually, whereas fossil fuel investments should dramatically decrease this decade to achieve this transition. Climate finance commitments also need to translate into action in the real economy, requiring all public and private actors to align their investments with Paris goals and net zero, sustainable pathways. This requires coordinated action from all actors:

Governments needs to build confidence in key markets with clear policy signals and incentives, with interim goals on net zero, whereas financial regulators should set standardized rules to enforce the targets

Development banks and international finance institutions can help build strategy, engage with counterparties, and support policy development, while deploying a wider range of instruments that take on more risk, helping to catalyze more private investment in developing economies

Private sector needs to better appreciate new approaches to collaborating and investing, but also needs to mainstream climate considerations by assessing risk and opportunities in a more holistic way

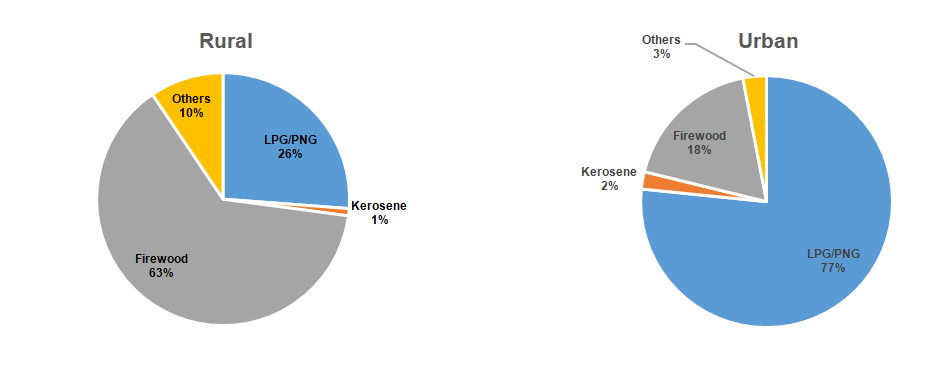

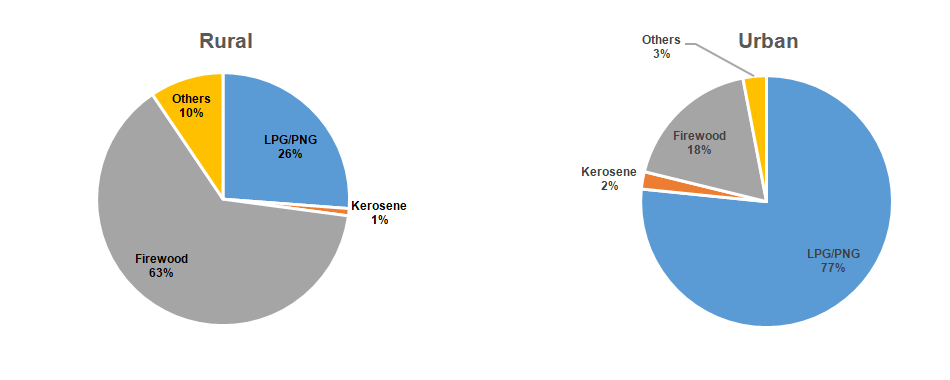

Approximately 40% (2.8 billion people) of the global population still cooks with either wood, dung, coal, or charcoal. Nearly 84% of rural Indian households cook on stoves that use solid or biomass fuels. In India, women spend an hour every day collecting firewood. This time dedicated to collecting firewood and cooking limits their ability to attend school and generate income. Moreover, women are exposed to toxic pollutants released from the burning of solid fuels (wood, charcoal, etc.).

Also, the burning of solid fuel in inefficient traditional stoves is responsible for the emission of various indoor air pollutants, which have direct and indirect impacts on the health of women and children. According to the Global Burden of Disease estimation, solid fuel burning for cooking accounted for 6 lakh premature deaths in 2019 in India. Thus, it is need of the hour to transition to electric cooking solutions which include access to electricity, and cleaner, more efficient stoves.

Benefits of Electric Cooking

Electric cooking is cost-effective, safer, more energy-efficient, requires less maintenance than conventional cooking methods, and is free of emissions. Additionally, Electric cooking can also make use of solar power in both urban and rural areas. Presently, about 24% of the electricity consumed in India is generated from renewable resources, and planning to expand it to 40% by 2030. This will be more viable in rural areas where the electricity grid may not be very reliable but solar energy is easier to provide.

Some of the key benefits of electric cooking are:

1

Speed – Cooks food 50% faster

2

Energy efficiency – savings in energy consumption and reduction energy usage cost

3

Easy & Precise Control – Achieve desired temperature

4

Safety – No flame, no gas leakage

5

Low maintenance –Change of burners, pipe, and regulators on periodic basis not required

6

Compact – Can be easily transferred from one place to another

7

Improves health – Prolonged exposure to smoke arising from conventional indoor cooking methods adversely impacting health

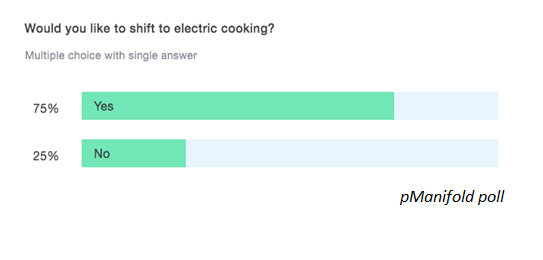

Despite the benefits of electric cooking only ~5% households use electric cooking devices today.

Moreover, there is a high willingness to shift to electric cooking, however, there are certain barriers which needs to be addressed. Let’s understand what are these barriers!

Barriers to transition to Electric cooking

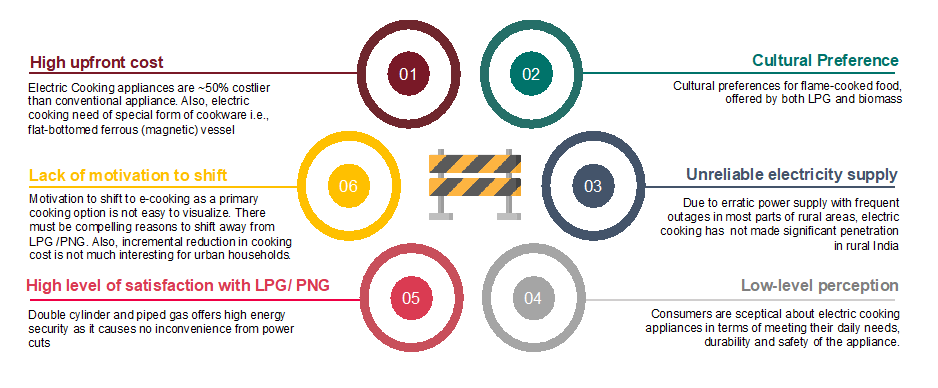

Getting consumers to adapt to new technology is a tricky proposition anywhere, but when it comes to electric cooking, its adoption remains riddled with more challenges. Affordability remains the topmost one, especially for a household that relies on biomass fuel which is available for free. An electric cook stove (induction to be precise)uses electromagnetism to heat cookware, which means that the utensils have to contain enough iron to generate a magnetic field around them. For a consumer, this not only means bearing upfront costs, as well as maintenance costs, but also the cost of switching to compatible cookware. This is something the majority of the households might not be willing to bear when their existing utensils and source of fuel are working to their convenience.90% of Ujjwala beneficiaries still use solid fuel for cooking.

The flame-based cooking offered by LPG and biomass is an important barrier that needs attention and resolution as chapatis, an integral food item of an Indian meal does not get cooked properly on an electric cookstove. According to a survey conducted by the Stockholm Environment Institute, majority of Indian women surveyed in rural area said they preferred cooking chapatis the traditional way in a clay oven, or over open fire, because it tastes better.

Another critical barrier is thelow-level perception for electric cooking mostly in rural areas. This issue is especially important, because it is this that is at the heart of the successful adoption of electric cooking technology. Consumers are sceptical about electric cooking appliances in terms of meeting their daily needs, durability and safety. Even though, firewood and LPG based cooking is quite unsafe.

In urban areas, there is lack of motivation to use electric cooking appliance. The incremental reduction in cooking cost is not of much interest as there is a high level of satisfaction and security in using LPG/ PNG.