Carbon markets are systems that allow for the trading of carbon credits or permits, which represent one metric ton of carbon dioxide (CO2), or an equivalent amount of another greenhouse gas (GHG) that has been reduced or removed from the earth’s atmosphere. It is not necessarily a carbon offset. A carbon credit only becomes a carbon offset when used for carbon offsetting, in other words, compensating for one’s GHG emissions. The idea behind carbon markets is to put a price on carbon emissions, creating an economic incentive for companies and individuals to reduce their emissions and invest in clean energy.

The evolution of carbon markets can be traced back to the 1990s, with the establishment of the first mandatory carbon market, the European Union Emissions Trading System (EU ETS) in 2005. The EU ETS operates as a cap-and-trade system, which limits the total amount of CO2 emissions from power plants and heavy industries and allows companies to buy and sell emissions allowances in order to meet their emissions targets.

In the following years, other countries and regions established their own carbon markets, including the Regional Greenhouse Gas Initiative (RGGI) in the northeastern United States, the Western Climate Initiative (WCI) in North America, and the carbon market established under the United Nations Framework Convention on Climate Change (UNFCCC), known as the Clean Development Mechanism (CDM).

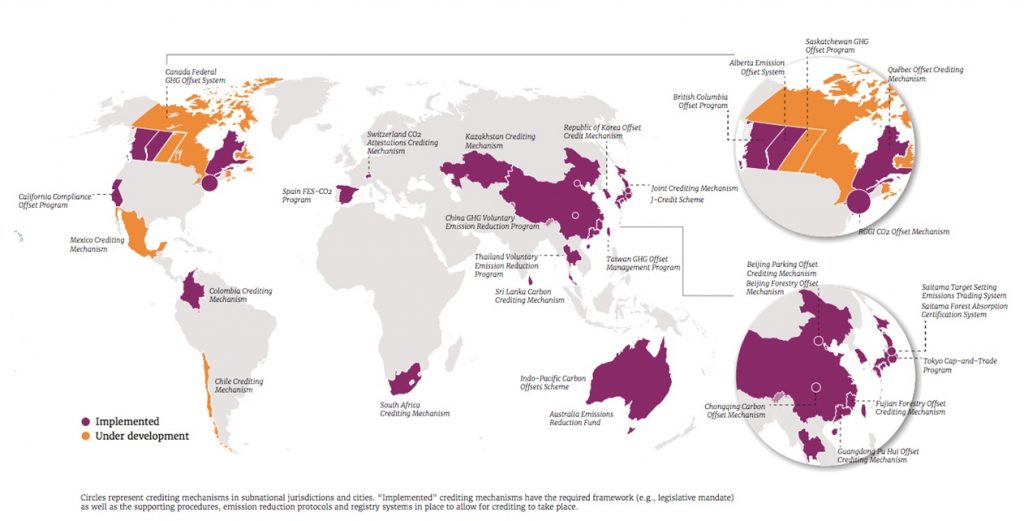

More recently, there has been an increasing interest in using carbon markets as a tool to help countries and regions meet their commitments under the Paris Agreement, which aims to limit global warming to well below 2 degrees Celsius. To this end, various carbon pricing initiatives and schemes have been launched worldwide. Some of them are already operational, such as California Cap and trade, Quebec Cap and trade and in Canada, carbon pricing policies are in place in seven provinces. In addition, there are also voluntary carbon markets, where companies, organizations, and individuals can purchase carbon credits to offset their emissions. These credits represent the reduction or removal of CO2 emissions from projects such as renewable energy or reforestation.

Different carbon pricing initiatives and schemes worldwide | by World Bank: https://openknowledge.worldbank.org/handle/10986/37455

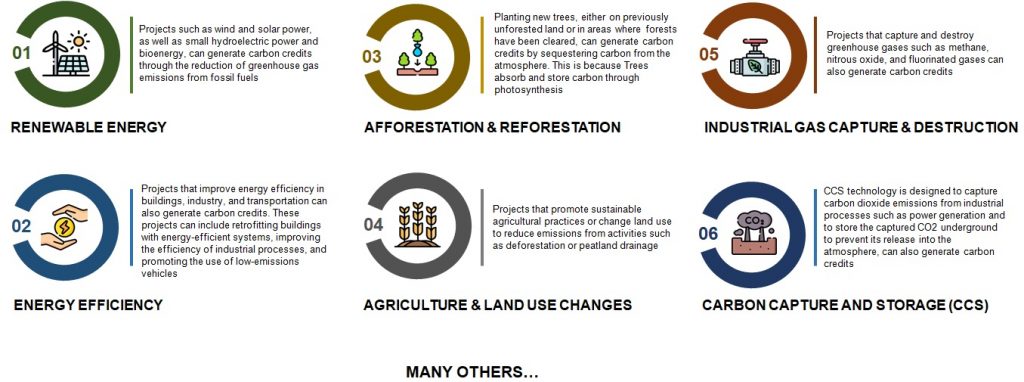

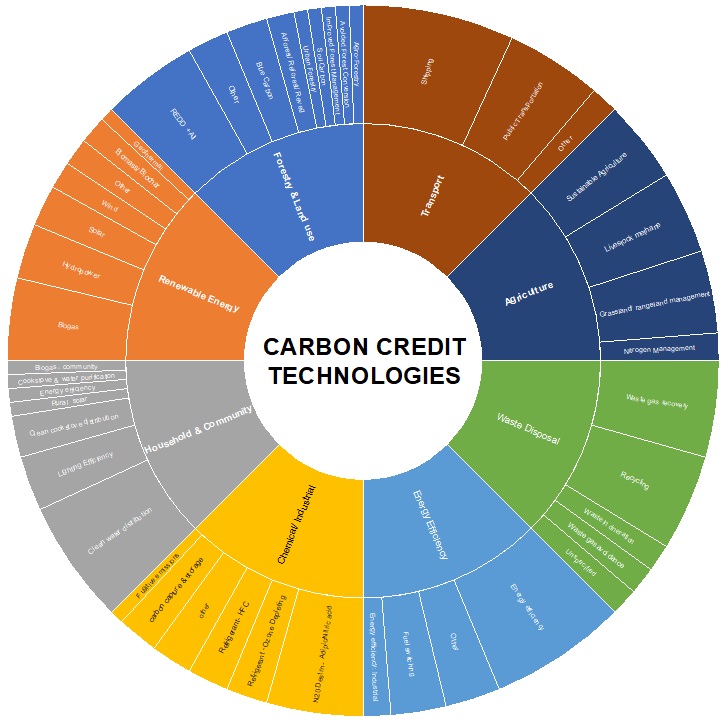

There are several technologies that can be used to generate carbon credits, including:

Different methods can be used to determine the value of a carbon credit, such as market conditions, cost of implementation, or the benefits of the project. The price can also depend on factors such as the type, size, and location of the project. The chart below shows an overview of the prices for different types of credits in the market as of January 2023.[i]

[i]https://8billiontrees.com/carbon-offsets-credits/new-buyers-market-guide/carbon-credit-pricing/

| Project Type | Volume Sold (MtCO2e) | Average Price ($) | Price Range ($) |

| Wind | 12.8 | 1.9 | 0.3 – 18 |

| REDD+ | 11 | 3.3 | 0.8 – 20+ |

| Landfill Methane | 7.9 | 2 | 0.2 – 19 |

| Tree planting | 3 | 7.5 | 2.2 – 20+ |

| Clean cookstoves | 3 | 4.9 | 2.0 – 20+ |

| Run-of-river hydro | 1.5 | 1.4 | 0.2 – 8 |

| Water/purification | 1.2 | 3.8 | 1.7 – 9 |

| Improved forest management | 0.8 | 9.6 | 2 – 17.5 |

| Biomass/biochar | 0.7 | 3 | 0.9 – 20+ |

| Energy efficiency -industrial-focused | 0.7 | 4.1 | 0.1 – 20 |

| Biogas | 0.6 | 5.9 | 1 – 20+ |

| Energy efficiency-community-focused | 0.6 | 9.4 | 3.3 – 20+ |

| Transportation | 0.5 | 29 | 2.2 – 6.8 |

| Fuel switching | 0.5 | 11.4 | 3.5 – 20+ |

| Solar | 0.3 | 4.1 | 1 – 9.8 |

| Livestock methane | 0.2 | 7 | 4.0 – 20+ |

| Geothermal | 0.1 | 4 | 2.5 – 8 |

| Agro-forestry | 0.1 | 9.9 | 9.0 – 11.0 |

Globally, carbon markets have evolved significantly over the past two decades and continue to be an important tool for reducing carbon emissions and combatting climate change. There is an increasing recognition of the need for carbon pricing as a mechanism to drive the transition to a low-carbon economy and many countries, regions and cities worldwide are implementing different form of carbon pricing mechanisms or planning to do so in the future.

The State of Carbon Market in India

India is the world’s third largest emitter of greenhouse gases (GHGs), after China and the US. India has been taking steps to implement a carbon market as part of its efforts to reduce greenhouse gas emissions and combat climate change. In India, carbon credits can be traded through various mechanisms, including the Clean Development Mechanism (CDM), which is an aspect of the United Nations Framework Convention on Climate Change (UNFCCC).

The CDM allows organizations in developed countries to invest in carbon reduction projects in developing countries, such as renewable energy projects in India, in order to offset their own GHG emissions. These investments help to fund the development of clean energy projects in developing countries, while also helping developed countries to meet their own emissions reduction targets.

India has been one of the largest recipients of CDM funding, with a large number of CDM projects registered in the country. These projects include renewable energy projects such as wind and solar power, as well as energy efficiency and afforestation projects. However, the CDM mechanism has been criticized for its lack of transparency, lack of long-term commitment, and failure to achieve large-scale emissions reductions.

Apart from CDM, India has started domestic carbon trading as well through its Carbon Emission Trading Scheme (ETS). It is still in early stage but allows companies to buy and sell carbon credits to other companies with the help of government. Between 2010 and June 2022, India issued 35.94 million carbon credits or nearly 17% of all voluntary carbon market credits issued globally. The market for carbon credits increased by 164% globally in 2021. It is anticipated to reach USD 100 billion by 2030.[i]

However, there are several challenges that need to be addressed in order to establish a functional and effective carbon market in India.

- One of the main challenges is the lack of a legal and regulatory framework for carbon trading. While India has announced its intent to establish a carbon market, it has not yet developed the necessary regulations and policies to govern the market. As per BEE recent announcement it is expected that in the year 2023, the framework will be rolled out and the voluntary market will be there. The compliance market will take time because targets and timelines need to be given to the industries. It is also expected the current Perform, Achieve and Trade (PAT) scheme would be transitioned into the compliance market. Moreover, Power exchanges which enable the trading of the energy saving certificates (ESCerts) converted from the excess energy savings, are likely to be the trading platform for carbon credits too, under the carbon market framework.[ii]

- Another challenge is the lack of accurate and reliable data on emissions. To establish a functional carbon market, accurate and verifiable data on emissions is necessary to establish baselines, set emissions targets and monitor compliance. However, in India, the lack of monitoring, reporting and verification (MRV) systems and data is seen as one of the major barriers to the successful implementation of a carbon market.

- Additionally, the initial setup costs for a carbon market, such as developing and implementing a carbon-pricing mechanism, building the necessary infrastructure and building the necessary systems for monitoring and enforcing compliance, can be substantial, and India lacks the sufficient resources and human capital to fully implement such mechanism. Moreover, the relatively low level of awareness and understanding of carbon markets among stakeholders in India can make it difficult to promote the market and ensure its success.

- Many sectors in India are still heavily dependent on fossil fuels and the lack of alternative energy sources as well as the lack of appropriate infrastructure to support alternative energy could make it difficult to implement a carbon market that would reduce emissions effectively.

Amidst the challenges, there are several opportunities for the growth of the carbon market in India, such as government support, the growing renewable energy sector, large emitting sectors, increasing corporate interest, international linkages, innovation, digitalization, domestic demand for carbon offsetting, and private sector participation. These factors create a conducive environment for the expansion of the carbon market in India, which can help address climate change and promote sustainable development

In conclusion, carbon market matters as it plays a vital role in addressing climate change by providing a mechanism to reduce greenhouse gas emissions. By creating a market for carbon, they incentivize companies and individuals to reduce emissions and invest in low-carbon technologies, while also allowing countries and companies to meet emissions reduction targets set by international agreements. They also mobilize private sector funding and expertise to support the transition to a low-carbon economy, promoting sustainable development and economic growth. Therefore, it is crucial to continue to develop and support carbon markets as a means to mitigate climate change.

[i]https://www.deccanherald.com/science-and-environment/carbon-credits-and-india-s-carbon-market-1163828.html

[ii]https://www.livemint.com/news/india/voluntary-carbon-trades-to-start-in-2023-11674498997601.html